Looking for the best SIPP provider in the UK? This guide compares the best SIPP platforms for low fees, ETFs, shares, funds and large pension pots. We’ve reviewed leading providers including InvestEngine, AJ Bell, Interactive Investor, Freetrade, Vanguard, Fidelity and Hargreaves Lansdown, and compared them on cost, investment choice, drawdown options and ease of use.

If you want the cheapest SIPP, InvestEngine stands out for ETF investors with zero platform fees. AJ Bell is one of the best choices for shares and ETFs thanks to its capped fees. Interactive Investor can work well for larger pension pots because of its flat monthly pricing. Vanguard is a strong option for passive investors who only want low-cost index funds.

The right SIPP depends on how much you have invested, what you want to buy, and whether you value low fees, wider investment choice or better retirement options such as drawdown.

Best SIPP providers at a glance

| Provider | Best For | Platform Fee | Trading Fee | Min. Invest |

|---|---|---|---|---|

| InvestEngine | Lowest cost | £0 (DIY) | £0 | £1 |

| AJ Bell | Shares/ETFs | 0.25% (cap £10/m) | £5 (£3.50 regular) | £1 |

| Interactive Investor | Larger pots | £5.99–£14.99/month flat | £3.99 | £1 |

| Freetrade | Free all-rounder | £0 (Basic plan) | £0 | £2 |

| Vanguard | Passive index | 0.15% (cap £375/year) | £0 | £100 |

| Fidelity | Funds/research | 0.35% (cap £7.50/month) | £7.50 | £1,000 |

| Hargreaves Lansdown | Widest range | 0.45% (first £250K) | £11.95 | £1 |

1. InvestEngine SIPP: best for lowest fees

InvestEngine removed all platform fees on its DIY SIPP in 2025, making it the cheapest pension provider in the UK. You pay absolutely nothing in platform charges, trading fees or withdrawal fees. The only cost is the underlying ETF charges (typically 0.03-0.20% annually).

The catch is that InvestEngine only offers ETFs, around 600 UK-listed options covering global equities, bonds, property, commodities and more. You cannot buy individual shares, mutual funds, investment trusts or bonds directly.

For most long-term pension investors, an ETF-only approach provides excellent diversification at the lowest possible cost. InvestEngine also offers managed portfolios and LifePlans for 0.25% if you prefer a hands-off approach.

The SIPP has limitations: transfer options are currently restricted, there are no employer contributions and drawdown options are basic. It suits accumulation-phase investors.

Best for: Cost-conscious investors happy with ETF-only investing who want to maximise pension growth by minimising fees.

2. AJ Bell SIPP: best for shares and ETFs

AJ Bell is a Which? Recommended SIPP Provider. The SIPP charges 0.25% annually, capped at £10 per month (£120/year) for shares, ETFs, investment trusts and bonds. This capped fee makes it particularly competitive for larger share portfolios.

The investment range is extensive: over 16,000 shares, 4,000 funds, 3,500 ETFs and bonds/gilts. Trading fees are £5 per deal, reducing to £3.50 for regular investments.

Best for: Investors wanting wide investment range with capped fees, particularly share-heavy portfolios above £50,000.

3. Interactive Investor SIPP: best for larger pots

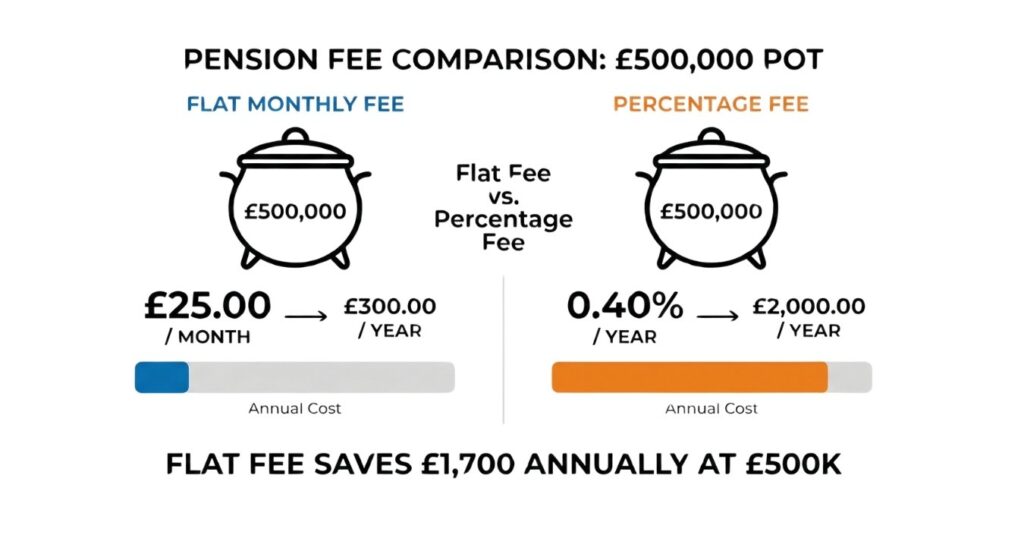

Interactive Investor uses a flat monthly fee: Core plan £5.99/month (pots up to £100,000), Plus plan £14.99/month (above £100,000). This becomes extraordinarily good value as your pension grows.

On a £500,000 SIPP, you pay £179.88/year with ii versus £1,750 with Hargreaves Lansdown. The platform offers over 40,000 investments and is a Which? Recommended Provider for SIPPs and drawdown.

Drawdown is comprehensive with no additional charges. Cash interest rates on uninvested SIPP balances are tiered from 2% to 3.25%.

Best for: Investors with pots above £50,000 wanting the widest choice at a predictable flat fee.

4. Freetrade SIPP: best free all-rounder

Freetrade now offers a free SIPP on its Basic plan with commission-free access to stocks, ETFs, mutual funds and gilts. The FX fee on Basic is 0.99% on non-GBP trades. Upgrading to Standard (£5.99/month) reduces this to 0.59%.

The platform supports in-specie transfers and is owned by IG Group (FTSE 250). Drawdown is not currently available and employer contributions are not accepted.

For how Freetrade compares to other free platforms, see our comparison.

Best for: Investors wanting a free SIPP with stocks, ETFs and mutual funds, especially those investing in UK-listed assets.

5. Vanguard SIPP: best for passive index investing

Vanguard charges 0.15% annually, capped at £375/year across all accounts. For pots up to £32,000, a flat £4/month applies. You can only invest in Vanguard’s own funds and ETFs.

The LifeStrategy range offers all-in-one portfolios and Target Retirement funds automatically adjust as you approach retirement. Ongoing fund charges are 0.06-0.22%.

Best for: Hands-off investors wanting a simple, low-cost pension using Vanguard’s index funds.

6. Fidelity SIPP: best for fund investors

Fidelity charges 0.35% on funds, with a flat £7.50/month for shares and ETFs. The Select 50 recommended fund list and analyst insights are excellent. A Which? Recommended SIPP Provider with comprehensive drawdown.

Best for: Fund-focused investors who value research tools and Fidelity’s low-cost index fund range.

7. Hargreaves Lansdown SIPP: widest range

The UK’s largest platform with £172 billion in assets. Fees are 0.45% on the first £250,000, with £11.95 per share trade. The widest investment range, best research and premium customer service come at the highest fees.

Best for: Investors prioritising the widest choice and premium service over lowest fees.

Which SIPP is cheapest for your pot size?

| Pot Size | Cheapest Provider | Annual Cost |

|---|---|---|

| Under £10,000 | InvestEngine | £0 (ETFs only) |

| £10K–£30K | InvestEngine | £0 (ETFs only) |

| £30K–£50K | InvestEngine or Freetrade | £0 |

| £50K–£100K | InvestEngine or Interactive Investor | £0 or £71.88 |

| £100K–£250K | InvestEngine or Interactive Investor | £0 or £179.88 |

| £250K+ | Interactive Investor | £179.88 |

How to choose a SIPP

Consider your pot size. Percentage-fee providers become expensive as your pension grows. Flat-fee and zero-fee providers save money on larger pots.

Consider what you want to invest in. ETFs only? InvestEngine. Individual shares? AJ Bell. Funds? Vanguard or Fidelity.

Consider pension transfers. Check for exit fees and valuable benefits before transferring. Most transfers take 2-6 weeks.

Consider drawdown. Interactive Investor, AJ Bell and Fidelity offer the most comprehensive drawdown services.

For tax-efficient investing alongside your pension, see our guides to the best stocks and shares ISAstocks and shares ISAs explained. Understanding your ISA allowance helps maximise both pension and ISA contributions.

SIPP FAQs

A Self-Invested Personal Pension lets you choose your own investments. You get income tax relief on contributions, tax-free investment growth, and can take 25% tax-free from age 57.

Basic rate taxpayers get 20% relief automatically. Higher rate (40%) and additional rate (45%) taxpayers claim extra through self-assessment. The annual limit is £60,000 or 100% of earnings, whichever is lower.

Usually yes, but check for valuable benefits you might lose, such as guaranteed annuity rates, protected pension age, or employer matching. Transferring to a low-cost SIPP could save thousands over time.

Currently from age 55, rising to 57 from April 2028. You can usually take 25% tax-free as a lump sum.

No. Neither Trading 212 nor eToro offers a SIPP. For commission-free pension investing, consider providers such as InvestEngine or Freetrade.

A common guideline is half your age as a percentage of salary. For example, if you start at 30, aim for 15% including employer contributions. The maximum with tax relief is £60,000 per year. Consider speaking to a financial adviser for personalised advice.

The value of pensions and investments can go down as well as up. Tax treatment depends on individual circumstances and may change. You may not be able to access pension savings until age 55 (rising to 57 from 2028). This guide is for informational purposes only and does not constitute financial advice.

Conclusion

The best SIPP provider in the UK is not the same for everyone. If you want the lowest possible cost and are happy investing only in ETFs, InvestEngine is hard to beat. If you want a broader investment range with competitive capped fees, AJ Bell is a strong all-round option. For larger pension pots, Interactive Investor’s flat-fee model can become very cost-effective. Passive investors who only want index funds may prefer Vanguard for its simplicity and low fees.

Before choosing a SIPP, compare total annual costs, the investments available, and whether the platform offers the retirement options you may need later, such as flexible drawdown.