To invest in the S&P 500 from the UK, open a Stocks and Shares ISA with a platform like Trading 212, InvestEngine, or Hargreaves Lansdown and buy a low-cost S&P 500 ETF such as Vanguard VUAG or iShares CSP1. Annual fund fees start from just 0.03%, and the S&P 500 has delivered an average annual return of around 10.3% since 1957. Hold within an ISA for completely tax-free growth on up to £20,000 per year.

The S&P 500 is the most widely followed stock market index in the world. It tracks 500 of the largest publicly listed companies in the United States, representing approximately 80% of the total US stock market by value. For UK investors looking to access global growth, the S&P 500 offers diversified exposure to some of the world’s most profitable businesses through a single, low-cost investment.

You cannot buy the S&P 500 index directly. Instead, UK investors access it through exchange-traded funds (ETFs) and index funds that track the index and are listed on the London Stock Exchange. There are currently 22 S&P 500 ETFs available to UK investors on the LSE, with annual fees ranging from just 0.03% to 0.15% (Source: justETF, February 2026).

The index delivered a total return of 17.9% in 2025, following gains of 25.0% in 2024 and 26.3% in 2023, marking three consecutive years of above-average performance (Source: First Trust Advisors, January 2026). Since its inception in 1957, the S&P 500 has delivered an average annual return of approximately 10.3%, though past performance is never a guarantee of future results.

This guide explains exactly how to invest in the S&P 500 from the UK, which ETFs to choose, what it costs, and how to minimise your tax bill.

Related: How to Start Investing in the UK (2026) | Best Stocks and Shares ISA UK (2026)

What Is the S&P 500 and Why Do UK Investors Buy It?

The S&P 500 (Standard and Poor’s 500) is a stock market index that measures the performance of 500 large-cap companies listed on US stock exchanges. It is weighted by market capitalisation, meaning the largest companies have the greatest influence on its performance. The index is maintained by S&P Dow Jones Indices, a division of S&P Global, and is rebalanced quarterly in March, June, September and December.

The index includes household names across 11 economic sectors, from technology giants like Apple, Microsoft and NVIDIA to consumer brands like Amazon and healthcare companies like UnitedHealth Group. As of early 2026, the top 10 holdings account for approximately 35% of the index’s total value, with technology stocks representing the largest sector weighting at around 34.5% (Source: BlackRock, January 2026).

UK investors are drawn to the S&P 500 for several reasons. The US stock market is significantly larger and more growth-oriented than the UK market, which is heavily weighted towards financials, energy and mining. The FTSE 100, by comparison, includes just 100 companies and has historically delivered lower long-term returns. The S&P 500 also provides exposure to sectors like technology and biotech that are underrepresented on the London Stock Exchange.

Investing in the S&P 500 is a passive strategy. Rather than picking individual stocks, you buy a fund that holds all 500 companies in proportion to their market size. This provides instant diversification, and the evidence strongly supports this approach. According to S&P Global’s SPIVA report (2024), more than 90% of actively managed funds fail to beat their benchmark index over a 15-year period.

Top 10 S&P 500 Holdings (as of early 2026)

| Company | Approximate Weighting |

|---|---|

| NVIDIA | 7.75% |

| Apple | 6.81% |

| Microsoft | 5.16% |

| Amazon | 3.41% |

| Alphabet (Class A) | 3.17% |

| Broadcom | 2.64% |

| Meta Platforms | 2.63% |

| Tesla | 2.04% |

| Berkshire Hathaway | 1.49% |

| JPMorgan Chase | 1.30% |

Source: Slickcharts.com/BlackRock, as of December 2025. Holdings are subject to change.

How to Invest in the S&P 500 from the UK: Step-by-Step

Investing in the S&P 500 from the UK is straightforward once you understand the process. You need a UK investment platform, an account type, and an S&P 500 ETF. Here is how to do it in six steps.

Step 1: Choose a UK investment platform.

Select an FCA-regulated platform that offers S&P 500 ETFs. Low-cost options include Trading 212, InvestEngine and Freetrade. Full-service options include Hargreaves Lansdown, AJ Bell and Interactive Investor. All provide access to S&P 500 ETFs listed on the London Stock Exchange.

Step 2: Open a Stocks and Shares ISA.

A Stocks and Shares ISA is the most tax-efficient way to invest in the S&P 500 from the UK. You can invest up to £20,000 per tax year, and all capital gains and dividends within the ISA are completely tax-free. If you have already used your ISA allowance, open a General Investment Account (GIA) instead.

Step 3: Verify your identity.

Your platform will ask for proof of identity (passport or driving licence) and proof of address. Most platforms complete verification within minutes using automated checks.

Step 4: Deposit funds.

Transfer money from your bank account to your investment platform. Most platforms accept bank transfer and debit card, with funds typically available to invest within one business day.

Step 5: Search for an S&P 500 ETF.

Search for your chosen ETF by name or ticker symbol. Popular options include Vanguard S&P 500 UCITS ETF (ticker: VUAG or VUSA), iShares Core S&P 500 UCITS ETF (ticker: CSP1), or SPDR S&P 500 UCITS ETF (ticker: SPY5).

Step 6: Place your buy order.

Enter the amount you want to invest and confirm the order. If your platform supports fractional shares, you can invest any amount from as little as £1. Otherwise, you will need enough to buy at least one whole ETF unit.

- Use a Stocks and Shares ISA for tax-free S&P 500 investing (£20,000 annual limit).

- Choose an FCA-regulated platform with low fees and S&P 500 ETFs listed on the LSE.

- Search for your ETF by ticker, such as VUAG, CSP1 or SPY5.

- You can start from as little as £1 on platforms offering fractional shares.

Which S&P 500 ETF Should UK Investors Choose?

Choosing the right S&P 500 ETF comes down to three factors: annual fees, whether the fund reinvests dividends automatically, and fund size. All the major S&P 500 ETFs track the same index, so performance differences are minimal. The key distinctions are cost, income handling and convenience.

There are two types of S&P 500 ETF: accumulating and distributing. An accumulating ETF (like VUAG or CSP1) automatically reinvests dividends back into the fund, increasing the value of your holding over time. A distributing ETF (like VUSA) pays dividends out as cash, typically quarterly. For long-term growth, most UK investors prefer accumulating ETFs because they benefit from compounding without needing to manually reinvest.

All of the ETFs below are domiciled in Ireland, which is important for tax efficiency. Under the Ireland-US tax treaty, these funds pay a reduced 15% withholding tax on US dividends, compared with the standard 30% rate that would apply to a UK-domiciled fund.

Best S&P 500 ETFs for UK Investors (2026)

| ETF Name | Ticker | TER | Type | Fund Size | Provider |

|---|---|---|---|---|---|

| Vanguard S&P 500 (Acc) | VUAG | 0.07% | Accumulating | £30.7B | Vanguard |

| Vanguard S&P 500 (Dist) | VUSA | 0.07% | Distributing | £35.7B | Vanguard |

| iShares Core S&P 500 (Acc) | CSP1 | 0.07% | Accumulating | £99.7B | BlackRock |

| SPDR S&P 500 (Acc) | SPY5 | 0.03% | Accumulating | Medium | State Street |

| Invesco S&P 500 (Acc) | SPXS | 0.05% | Accumulating | Medium | Invesco |

| iShares S&P 500 GBP Hedged | GSPX | 0.20% | Accumulating | Medium | BlackRock |

Source: JustETF, fund provider websites, verified February 2026. TER = Total Expense Ratio. All funds are UCITS-compliant and domiciled in Ireland.

For most UK beginners, Vanguard VUAG is the simplest choice. It costs 0.07% per year, reinvests dividends automatically, is physically replicated, and is widely available across all major UK platforms. At a share price of around £100 (as of early 2026), it is also accessible without needing fractional shares.

For the lowest fees, SPDR SPY5 charges just 0.03% per year. On a £10,000 investment, that is just £3 per year compared with £7 for Vanguard or iShares. Over decades, this small difference can compound, though fund size and liquidity are also worth considering.

iShares CSP1 is the largest S&P 500 ETF in the world with nearly £100 billion in assets, making it extremely liquid with tight bid-ask spreads. However, its share price is significantly higher than VUAG, which may matter if your platform does not offer fractional shares.

- Vanguard VUAG (0.07% fee, accumulating) is the most popular choice for UK ISA investors.

- SPDR SPY5 offers one of the lowest fees at just 0.03% per year.

- All major S&P 500 ETFs track the same index, so performance differences are typically negligible.

- Choose accumulating (Acc) for long-term growth and distributing (Dist) if you want regular income.

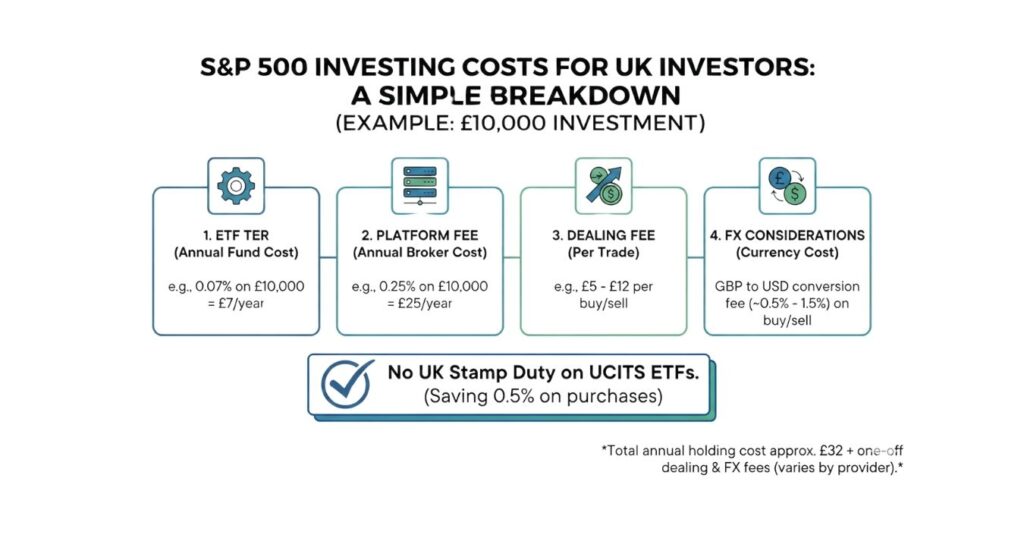

What Does It Cost to Invest in the S&P 500 from the UK?

The total cost of investing in the S&P 500 from the UK includes three main components: the ETF’s annual fee, your platform’s charges, and any currency conversion fees. Understanding all three helps you keep more of your returns.

ETF annual fee (TER).

This is the fund manager’s charge for running the ETF. S&P 500 ETFs are among the cheapest investment funds available, with fees ranging from 0.03% to 0.15% per year. On a £10,000 investment in VUAG (0.07% TER), you would pay approximately £7 per year.

Platform fees.

Your investment platform may charge a dealing fee per trade, an annual platform fee, or both. Trading 212 and InvestEngine charge zero platform fees for ETF investing. Hargreaves Lansdown charges up to 0.45% per year on funds, while Interactive Investor charges a flat £5.99 per month.

Currency conversion (FX) fees.

The S&P 500 ETFs listed above are priced in GBP on the London Stock Exchange, so you buy them in pounds. The FX conversion happens at the fund level. Sticking to GBP-denominated tickers (VUAG, VUSA, CSP1) on the LSE avoids additional platform FX charges.

No stamp duty.

Unlike buying individual UK shares, which attract 0.5% Stamp Duty Reserve Tax, ETFs domiciled in Ireland are exempt from UK stamp duty (Source: HMRC).

Cost Comparison: £10,000 Invested in S&P 500

Cost Comparison: Buying VUAG on Different Platforms (First Year)

| Cost Type | Trading 212 + VUAG | HL + VUAG | ii + VUAG |

|---|---|---|---|

| ETF fee (0.07%) | £7/year | £7/year | £7/year |

| Platform fee | £0 | £45/year (0.45%) | £71.88/year (£5.99/month) |

| Dealing fee | £0 | £11.95 per trade | £3.99 per trade |

| Total first-year cost | £7 | £64 | £83 |

Source: Platform websites, February 2026. Costs assume a single buy trade and one year of holding.

Related: Best Trading Platforms UK (2026) | Trading 212 Review (2026)

S&P 500 vs FTSE 100: Which Is Better for UK Investors?

This is one of the most common questions UK investors ask, and the answer depends on your goals and existing portfolio exposure. Both indices have distinct characteristics that make them suitable for different purposes.

The S&P 500 has significantly outperformed the FTSE 100 over the long term, driven largely by the dominance of US technology companies. The FTSE 100 has delivered more modest capital growth but offers a higher dividend yield, currently around 3.5% to 4.0% compared with approximately 1.3% to 1.5% for the S&P 500.

The FTSE 100 is more concentrated in old economy sectors such as oil and gas (Shell, BP), banking (HSBC, Barclays), mining (Rio Tinto, Glencore) and consumer staples (Unilever, Diageo). The S&P 500 is dominated by technology and growth companies, with information technology alone accounting for approximately 34.5% of the index.

For UK investors, there is also a currency dimension. The S&P 500 is denominated in US dollars, so when you invest through an unhedged ETF, your returns are affected by movements in the GBP/USD exchange rate. Over the very long term, currency movements tend to wash out, but they can create significant short-term volatility.

Many experienced investors hold both, using the S&P 500 for growth and the FTSE 100 for income and domestic currency exposure. A common starting allocation for UK investors is a global equity fund or a combination of S&P 500 and FTSE exposure.

What Are the Tax Implications for UK Investors?

Understanding the tax treatment of S&P 500 investments is essential for maximising your returns. The tax you pay depends entirely on which account type you use.

Stocks and Shares ISA.

This is the simplest and most tax-efficient option. All capital gains and dividends within an ISA are completely free from UK tax. You can invest up to £20,000 per tax year (2025/26). For most UK investors building long-term wealth through S&P 500 ETFs, an ISA should be the first choice.

Self-Invested Personal Pension (SIPP).

Investing through a SIPP provides tax relief on your contributions. A basic-rate taxpayer effectively gets a 25% government bonus, so a £100 contribution costs only £80. However, pension funds are locked until age 57 (rising from 55 in 2028), and withdrawals above the 25% tax-free lump sum are taxed as income.

General Investment Account (GIA).

If you have used your ISA allowance, a GIA offers unlimited investment but no tax shelter. Capital gains above the £3,000 annual exempt amount (2025/26, down from £12,300 in 2022/23) are taxed at 18% for basic-rate taxpayers or 24% for higher-rate taxpayers (Source: HMRC, from 30 October 2024). Dividends above the £1,000 annual allowance are taxed at 8.75%, 33.75% or 39.35% depending on your tax band.

US withholding tax.

S&P 500 ETFs domiciled in Ireland benefit from the Ireland-US tax treaty, which reduces the US dividend withholding tax from 30% to 15%. This is applied at the fund level before dividends reach UK investors. Within an ISA, UK investors cannot reclaim this 15% withholding, but the overall tax saving compared with a non-treaty rate is significant.

- A Stocks and Shares ISA makes S&P 500 returns completely tax-free in the UK.

- Ireland-domiciled ETFs automatically benefit from the reduced 15% US withholding tax.

- The CGT annual exempt amount is £3,000 for 2025/26, making ISA investing even more important.

- Accumulating ETFs such as VUAG and CSP1 can be more tax-efficient in a GIA as they defer dividend income.

Related: Capital Gains Tax on Shares UK (2026) | Stocks and Shares ISA Explained (2026)

What Are the Risks of Investing in the S&P 500?

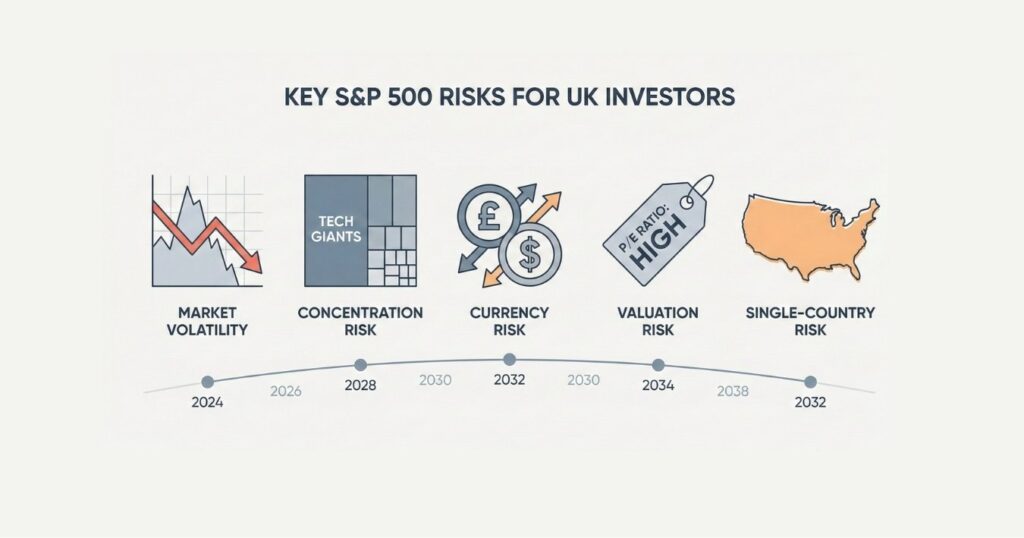

The S&P 500 has delivered strong long-term returns, but it is not a risk-free investment. Understanding the key risks helps you make informed decisions and stay invested during difficult periods.

Market risk.

Stock markets go down as well as up. The S&P 500 has experienced a decline of at least 10% roughly every two and a half years on average (Source: Capital Group). During the COVID-19 crash in March 2020, the index fell approximately 34% in just over a month. In the first half of 2025, the index dropped nearly 19% amid tariff-related volatility before recovering to finish the year up 17.9% (Source: First Trust Advisors, January 2026).

Concentration risk.

The so-called Magnificent Seven stocks (Apple, Microsoft, NVIDIA, Alphabet, Amazon, Meta and Tesla) account for approximately 35% of the index’s total value (Source: Motley Fool, January 2026). If the technology sector experiences a sustained downturn, the impact on the S&P 500 would be significant.

Currency risk.

As a UK investor buying a USD-denominated index, your returns are affected by changes in the GBP/USD exchange rate. GBP-hedged ETFs such as iShares GSPX (TER: 0.20%) remove this currency exposure, but hedging costs can reduce returns over time.

Valuation risk.

The S&P 500 currently trades at a forward price-to-earnings ratio of approximately 22x, matching the peak multiple seen in 2021 and approaching the record 24x in 2000 (Source: Goldman Sachs, January 2026). High valuations suggest future returns may be more moderate than the past three years.

Single-country risk.

The S&P 500 provides exposure solely to US companies. Investors seeking broader global diversification may prefer a global index fund such as FTSE All-World or MSCI World alongside their S&P 500 allocation.

Despite these risks, time has historically been the most effective risk management tool. The S&P 500 has delivered a positive return in approximately 79% of calendar years since 1993, and about three out of four years have been positive on a total return basis since 1928 (Source: Visual Capitalist, January 2026).

Should You Invest in the S&P 500 or a Global Fund?

The S&P 500 gives you exposure to 500 large US companies. A global fund, such as a Vanguard FTSE All-World ETF (ticker: VWRL or VWRP), holds thousands of companies across developed and emerging markets worldwide. Both are excellent passive investments, but they serve different purposes.

The S&P 500 has outperformed most global indices over the past decade, driven by the strength of US technology companies. However, this outperformance is partly reflected in higher valuations. The US currently accounts for approximately 60% to 65% of global stock market capitalisation, so even a global fund gives you significant US exposure.

A global fund provides built-in diversification across countries, currencies and economic cycles. If the US market underperforms relative to the rest of the world in future years, as it did during the 2000s, a global fund would capture gains from other regions that an S&P 500 fund would miss.

For beginners, a common approach is to start with a single global index fund for maximum simplicity, or to split between an S&P 500 ETF and a FTSE All-World ETF. There is no objectively correct answer, and many successful portfolios include both.

Currency Hedging: Do UK Investors Need It?

Currency hedging removes the impact of exchange rate movements between GBP and USD on your investment returns. For UK S&P 500 investors, this means your returns would mirror the US dollar performance of the index, regardless of what happens to the pound.

GBP-hedged S&P 500 ETFs are available, including the iShares S&P 500 GBP Hedged UCITS ETF (GSPX, TER: 0.20%) and the Xtrackers S&P 500 GBP Hedged UCITS ETF (XDPG, TER: 0.09%). These ETFs use currency derivatives to neutralise the GBP/USD exchange rate effect.

However, hedging comes at a cost. The higher TER on hedged ETFs and the implicit cost of rolling currency contracts reduce your returns over time. For investors with a time horizon of 10 years or more, most evidence suggests that currency movements tend to even out and that the additional cost of hedging is not justified.

Hedging may make sense for investors with a shorter time horizon (under five years), those who are particularly risk-averse, or those who have a specific view that the pound will strengthen significantly against the dollar. For most long-term UK investors, an unhedged ETF such as VUAG or CSP1 is the standard choice.

Frequently Asked Questions

You can invest from as little as £1 if your platform offers fractional shares. Trading 212 and InvestEngine both support fractional ETF investing. Without fractional shares, you need enough to buy one whole ETF unit, which is approximately £100 for Vanguard VUAG or around £550 for iShares CSP1 (as of early 2026).

All major UK investment platforms are regulated by the FCA and covered by the FSCS, which protects up to £85,000 per firm if your platform fails. ETF holdings are held separately from the platform’s own assets in nominee accounts. However, the value of investments can go down as well as up.

Vanguard VUAG is one of the most popular choices among UK ISA investors. It charges 0.07% per year, reinvests dividends automatically and is widely available on UK platforms. SPDR SPY5 charges 0.03% per year and is among the lowest-cost options.

Not if you hold your investment within a Stocks and Shares ISA. ISA investments are free from UK capital gains tax and dividend tax. Outside an ISA, gains above £3,000 (2025/26) may be subject to capital gains tax, and dividends above £1,000 may be taxed at your marginal rate.

Both track the same S&P 500 index with the same 0.07% annual fee. VUAG reinvests dividends automatically for long-term growth, while VUSA pays dividends out as cash quarterly for income.

Yes. You can buy S&P 500 ETFs through a Self-Invested Personal Pension (SIPP). Contributions receive tax relief, meaning a basic-rate taxpayer effectively receives a 25% government top-up. Many UK SIPP providers offer access to S&P 500 ETFs.

Regular investing, often called pound-cost averaging, is a common strategy. By investing a fixed amount monthly, you reduce the impact of market volatility. Most UK platforms allow automatic monthly investments into S&P 500 ETFs.

The S&P 500 has delivered an average annual return of around 10% per year since 1957, including dividends. However, returns vary significantly from year to year and past performance does not guarantee future results.

Timing the market is extremely difficult and generally not recommended for long-term investors. While forecasts may suggest positive returns, valuations can fluctuate. For long-term investors, staying invested consistently is typically more effective than trying to time entry points.

Your ETF holdings are held in segregated nominee accounts separate from the platform’s own finances. If the platform fails, your investments can be transferred to another provider. The FSCS protects up to £85,000 per firm for eligible claims.

Related Reading

- How to Start Investing in the UK (2026) — Complete beginner’s guide to building your first portfolio

- How to Buy Shares in the UK (2026) — Step-by-step guide to buying individual shares and ETFs

- Best Stocks and Shares ISA UK (2026) — Compare the top ISA platforms for tax-free investing

- Best Trading Platforms UK (2026) — Full comparison of UK investment platforms and fees

Risk Disclaimer: Investments can go down as well as up in value, and you may get back less than you invest. Tax treatment depends on your individual circumstances and may change in the future. This article does not constitute personal financial advice. If you are unsure about the suitability of an investment, seek advice from a qualified financial adviser.