UK investors can short stocks using CFDs (Contracts for Difference) or spread betting through FCA-regulated brokers like IG, CMC Markets or City Index. Spread betting profits are tax-free, while CFD gains are subject to capital gains tax. Short selling is high-risk: between 70% and 80% of retail CFD accounts lose money (Source: FCA). You cannot short stocks inside an ISA or SIPP.

Short selling means betting that a share price will fall. If you believe a company is overvalued or heading for trouble, shorting allows you to profit from the decline rather than simply watching from the sidelines.

In the UK, short selling is legal and regulated by the Financial Conduct Authority (FCA). Retail investors typically short stocks using CFDs or spread betting rather than borrowing and selling physical shares, which is generally reserved for institutional investors.

This guide explains how short selling works, the different methods available to UK investors, the costs and tax implications, and the significant risks you need to understand before placing a short trade.

Warning: Short selling carries substantially higher risk than traditional investing. Your potential losses are theoretically unlimited because a share price can rise indefinitely. Between 70% and 80% of retail CFD accounts lose money (Source: FCA, PS19/18). This guide is for educational purposes only. Never short with money you cannot afford to lose.

What Is Short Selling and How Does It Work?

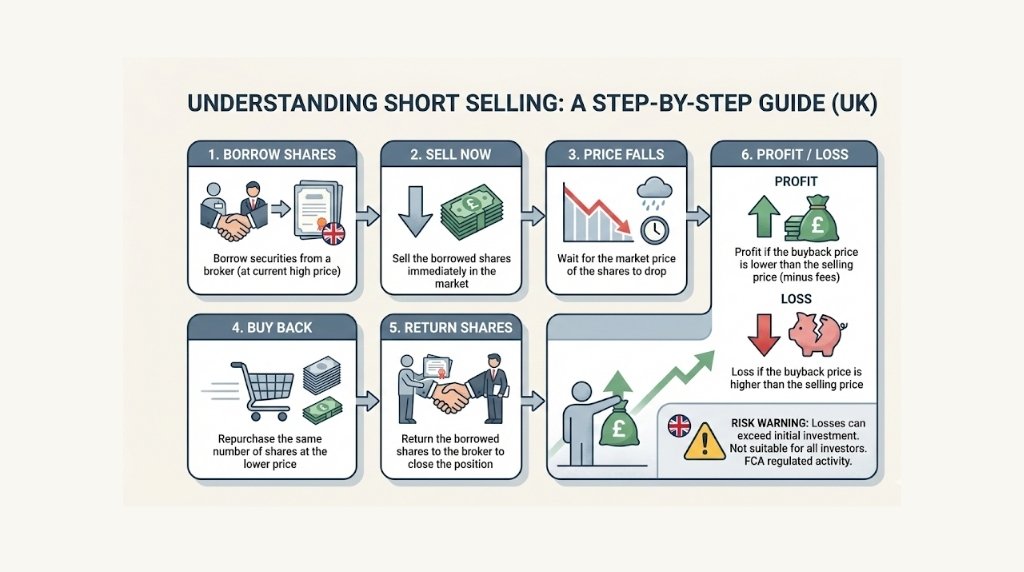

In traditional investing, you buy shares hoping they will rise in value. Short selling reverses this: you sell first and buy back later, profiting if the price falls.

The basic mechanics work like this:

- You borrow shares from a broker and immediately sell them at the current market price.

- You wait for the price to fall.

- You buy the shares back at the lower price and return them to the broker.

- The difference between your selling price and your buying price is your profit, minus fees.

In practice, UK retail investors rarely borrow physical shares. Instead, they use derivative products like CFDs and spread bets that replicate the economics of short selling without the need to borrow the underlying shares.

Short Selling Example

Suppose you believe a FTSE 250 company trading at 500p per share is overvalued. You open a short CFD position equivalent to 1,000 shares at 500p.

- If the price falls to 400p, you close the position. Your profit is 100p x 1,000 = £1,000 (before fees).

- If the price rises to 600p, your loss is 100p x 1,000 = £1,000 (plus fees).

- If the price rises to 800p, your loss would be 300p x 1,000 = £3,000, and the price could continue rising.

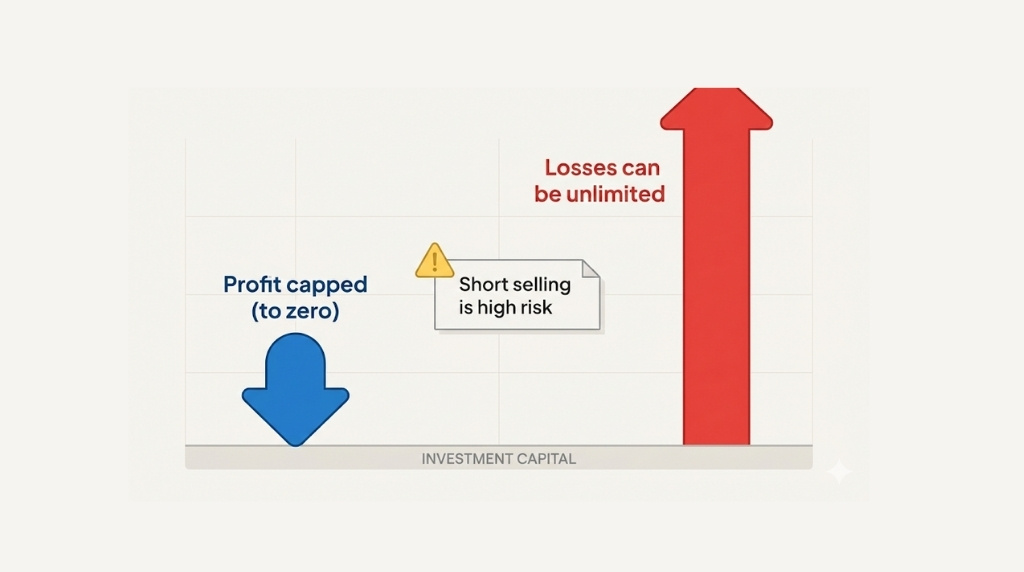

This is the fundamental danger of shorting: your profit is capped (a share can only fall to zero) but your loss is theoretically unlimited.

- Short selling reverses normal investing. You profit when prices fall and lose when prices rise. Because there is no ceiling on how high a share price can go, your potential losses when shorting are unlimited.

4 Ways to Short Stocks in the UK

UK investors have four main methods for shorting. Each has different costs, tax treatment and complexity.

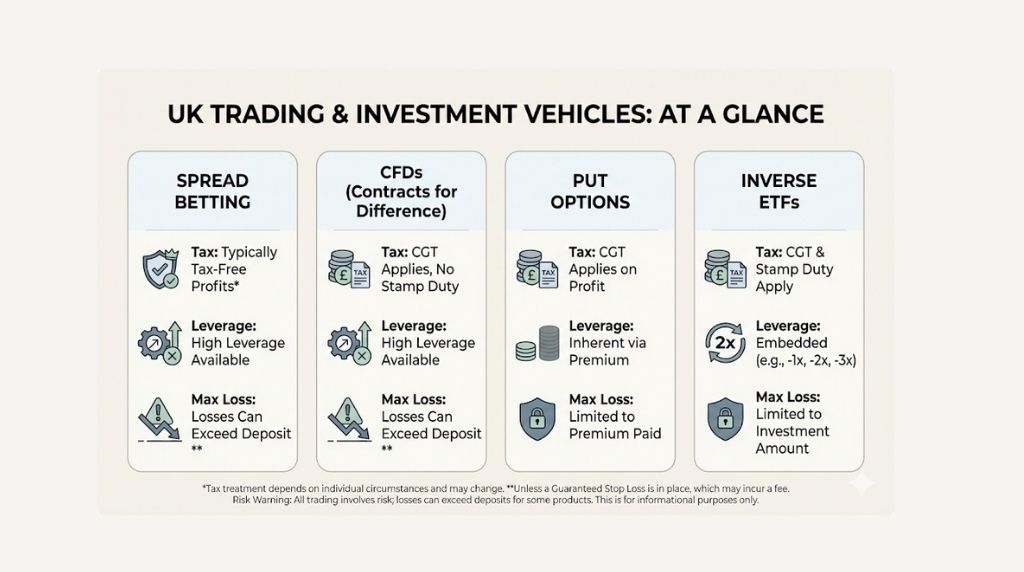

1. Spread Betting

Spread betting is the most popular method for UK retail investors to short stocks. You bet a certain amount per point of price movement. If you bet £5 per point and the share price falls 50 points, you make £250.

The key advantage of spread betting is tax treatment. HMRC classifies spread betting as gambling, so profits are completely tax-free: no capital gains tax, no income tax and no stamp duty (Source: HMRC, July 2025). You also benefit from FCA-mandated negative balance protection, meaning you cannot lose more than the funds in your account.

Leverage: Spread betting uses leverage, so you only need a fraction of the full position value as a margin deposit. FCA rules cap leverage at 5:1 for individual shares (20% margin) and 20:1 for major indices (Source: FCA, PS19/18, August 2019).

Best for: UK tax residents who want tax-free short-term trading. The most cost-effective way to short for most retail traders.

2. CFDs (Contracts for Difference)

A CFD is a contract between you and your broker. You agree to exchange the difference in the share price between when you open and close the position. To short using a CFD, you open a 'sell' position.

Unlike spread betting, CFD profits are subject to capital gains tax. However, CFD losses can be offset against other capital gains, which can be useful for hedging. CFD pricing follows the actual share price rather than a points-based system, which some traders prefer for clarity.

Leverage: The same FCA leverage caps apply: 5:1 for individual shares and 20:1 for major indices. Negative balance protection is mandatory for all UK retail CFD accounts.

Best for: Traders who want to offset losses against gains for tax purposes, or who prefer pricing that directly mirrors share prices.

3. Put Options

A put option gives you the right (but not the obligation) to sell a share at a specific price by a certain date. If the share price falls below that level, the option becomes profitable. If the price stays above that level, you lose only the premium you paid for the option.

Put options are available through brokers like Interactive Brokers and Saxo. They are less commonly used by UK retail investors because the options market for UK shares is relatively limited compared to US markets.

Best for: More experienced traders who want a defined maximum loss (the option premium). Useful for hedging existing share positions.

4. Inverse ETFs

Inverse ETFs are exchange-traded products that move in the opposite direction to an index. For example, an inverse FTSE 100 ETF rises when the FTSE 100 falls. Some inverse ETFs are leveraged (2x or 3x), amplifying both gains and losses.

Inverse ETFs can be bought through standard share dealing accounts and some ISA providers, although most leveraged products are not eligible for ISAs. They are designed for short-term trading and can lose value over time even if the underlying index is flat, due to daily rebalancing effects.

Best for: Investors who want short-term bearish exposure without using a CFD or spread betting account.

Methods to Profit From Falling Markets

| Method | Tax Treatment | Leverage | Max Loss | Account Needed |

|---|---|---|---|---|

| Spread Betting | Tax-free (HMRC) | Up to 5:1 (shares) | Limited to account funds | Spread betting account |

| CFDs | CGT applies | Up to 5:1 (shares) | Limited to account funds | CFD account |

| Put Options | CGT applies | No (premium paid upfront) | Premium paid only | Options-enabled account |

| Inverse ETFs | CGT applies (unless in ISA) | 1x, 2x or 3x | Amount invested | Share dealing or ISA |

- For most UK retail traders, spread betting is the simplest and most tax-efficient way to short stocks. CFDs are better if you want to use losses for tax offsetting. Put options and inverse ETFs suit specific situations.

How to Short a Stock in the UK: Step by Step

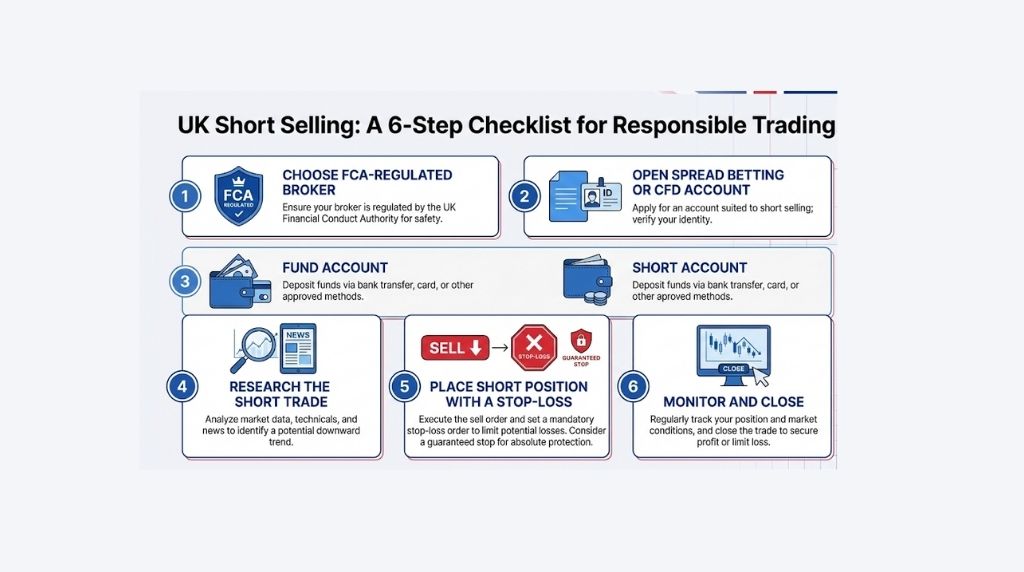

Step 1: Choose an FCA-Regulated Broker

Only use brokers authorised and regulated by the FCA. Check the FCA Financial Services Register to verify any broker before depositing funds. Popular FCA-regulated brokers for short selling include:

- IG: The UK's largest spread betting and CFD provider. Over 17,000 markets. Founded 1974.

- CMC Markets: Low spreads, strong platform. Listed on the London Stock Exchange.

- City Index: Good for beginners. Part of the StoneX Group.

- Spreadex: Combines financial and sports spread betting. Competitive share spreads.

- Interactive Brokers: Best for options and direct market access. Suited to experienced traders.

Step 2: Open a Spread Betting or CFD Account

Short selling is not available through standard stocks and shares ISA or SIPP accounts. You need to open a dedicated spread betting or CFD account. The application process requires identity verification, proof of address and a risk assessment questionnaire about your trading experience.

Step 3: Fund Your Account

Most brokers require a minimum deposit of between £100 and £500. Only deposit money you can afford to lose entirely. Bank transfer and debit card are the most common funding methods.

Step 4: Research Your Short Trade

Identify the stock you believe will fall. Consider fundamental factors (overvaluation, poor earnings, declining revenue) and technical signals (overbought conditions, broken support levels). Avoid shorting solely based on tips or social media posts.

Step 5: Place Your Short Trade

Search for the stock on your broker's platform and select 'Sell' or 'Short'. Set your position size carefully. For spread betting, this is your stake per point. For CFDs, it is the number of shares. Always set a stop-loss to limit your potential loss, and consider using a guaranteed stop-loss (GSLO) for extra protection in volatile markets.

Step 6: Monitor and Close Your Position

If the price falls as expected, close the position to lock in your profit. If the price moves against you and hits your stop-loss, the position closes automatically. Never remove or widen a stop-loss to avoid taking a loss.

Tax Rules for Short Selling in the UK

The tax treatment depends entirely on which method you use.

Spread Betting: Tax-Free

HMRC classifies spread betting as gambling. Profits are exempt from capital gains tax, income tax and stamp duty. However, this also means losses cannot be offset against other gains (Source: HMRC, BIM22017, July 2025).

CFDs: Capital Gains Tax Applies

CFD profits are subject to capital gains tax at 18% (basic rate) or 24% (higher rate) for 2025/26 (Source: HMRC, 2025/26). You can offset CFD losses against other capital gains in the same tax year. The annual CGT allowance of £3,000 applies. See our full capital gains tax guide for details.

Put Options and Inverse ETFs

Both are subject to capital gains tax. Inverse ETFs held in an ISA may be tax-free, but most leveraged products are not ISA-eligible. Standard dividend tax rules apply to any distributions.

What Does It Cost to Short a Stock in the UK?

Short selling involves several costs beyond the basic trade:

The spread. The difference between the buy and sell price. This is the primary cost of every trade. Tighter spreads mean lower costs. Major FTSE 100 shares typically have tighter spreads than small-cap stocks.

Overnight financing. If you hold a short position overnight, your broker charges a daily financing fee (sometimes called a swap rate). This is typically based on the interbank rate plus a markup. For a £5,000 position, overnight costs might be £0.50 to £1.50 per night. These costs add up quickly for longer-term positions.

Guaranteed stop-loss premium. If you use a guaranteed stop-loss order, brokers charge a small additional premium. This guarantees your exit price even in fast-moving or gapping markets.

Commission (some CFD brokers). Some CFD brokers charge a commission per trade in addition to the spread, particularly on share CFDs. This is typically 0.08% to 0.10% of the position value.

Dividend adjustments. If the company pays a dividend while you are short, the dividend amount is deducted from your account. This is an additional cost that many beginners overlook.

Risks of Short Selling

Short selling is one of the highest-risk activities available to retail investors. Understand these risks before placing a single trade.

Unlimited loss potential. When you buy a share, your maximum loss is the amount you invested (it can only fall to zero). When you short, the price can rise indefinitely. A £500 short can generate thousands in losses if the price surges.

Short squeezes. If a heavily shorted stock suddenly rises, short sellers rush to buy back shares to limit losses. This buying pressure pushes the price even higher, creating a vicious cycle. The GameStop short squeeze in January 2021 saw the share price rise from roughly $20 to $483 in weeks, causing billions in losses for short sellers.

Leverage amplifies losses. With 5:1 leverage on shares, a 20% rise against your position wipes out your entire margin deposit. While FCA-mandated negative balance protection prevents you losing more than your account balance, losing your full deposit is a real possibility.

Overnight and weekend risk. Markets can gap significantly overnight or over weekends due to news events. Your standard stop-loss may not protect you from a gap (only guaranteed stop-losses cover this).

High failure rate. The FCA requires all CFD brokers to display the percentage of retail accounts that lose money. The typical figure is between 70% and 80% (Source: FCA, PS19/18). This means the clear majority of retail traders shorting via CFDs and spread bets lose money overall.

Psychological difficulty. Shorting goes against the natural optimism bias of markets. It can be emotionally challenging to hold a losing short position when the stock keeps rising and market sentiment is bullish.

- Short selling is not a strategy for beginners. If you are new to investing, focus on long-term investing through index funds and ISAs before considering any form of short selling. Only experienced traders with a clear risk management plan should attempt to short stocks.

Who Should and Should Not Short Stocks?

Short Selling May Suit You If:

- You have significant trading experience and understand leverage, margin and risk management.

- You have a specific, well-researched reason to believe a stock will fall (not just a hunch).

- You only use money you can afford to lose entirely.

- You always use stop-losses and never risk more than 1% to 2% of your account on a single trade.

- You want to hedge an existing long portfolio against a market downturn.

Short Selling Is Probably Not For You If:

- You are a beginner investor. Start with how to start investing instead.

- You do not fully understand how leverage and margin calls work.

- You cannot afford to lose your entire deposit.

- You are investing for long-term goals like retirement. A stocks and shares ISA or SIPP is far more appropriate.

- You are tempted by social media tips or 'guaranteed' short selling signals.

Frequently Asked Questions

Yes. Short selling through CFDs and spread betting is legal in the UK when conducted through FCA-authorised brokers. The FCA regulates these activities and requires brokers to provide negative balance protection and standardised risk warnings (Source: FCA, PS19/18, August 2019).

No. Short selling is not permitted within stocks and shares ISAs or SIPPs. These tax-efficient accounts are designed for long-term investing and only allow long positions in approved assets. You need a separate spread betting or CFD account to short stocks.

Spread betting is typically the cheapest option for UK residents because profits are tax-free and most brokers charge no commission beyond the spread. For larger or longer-term positions, compare overnight financing costs across brokers before choosing.

Most UK brokers require a minimum deposit of £100 to £500 for a spread betting or CFD account. However, you should only short with money you can afford to lose entirely. Starting with a demo account is strongly recommended.

A short squeeze occurs when a heavily shorted stock suddenly rises in price. Short sellers rush to buy back shares to close their positions, which pushes the price even higher. This can cause rapid, dramatic price increases and significant losses for anyone holding a short position.

Both allow you to short stocks, but they differ in tax treatment. Spread betting profits are tax-free in the UK; CFD profits are subject to capital gains tax. CFD losses can be offset against other gains, while spread betting losses cannot. Spread betting uses a points-based system; CFDs mirror actual share prices.

Under FCA rules (since August 2019), all UK retail CFD and spread betting accounts must have negative balance protection. This means you cannot lose more than the funds in your trading account. However, you can still lose your entire deposit.

The FCA caps leverage for retail investors at 5:1 for individual shares (20% margin), 10:1 for non-major indices, 20:1 for major indices like the FTSE 100, and 30:1 for major currency pairs (Source: FCA, PS19/18).

No. Most financial experts advise beginners to build a solid foundation in long-term investing first. Between 70% and 80% of retail CFD accounts lose money. If you are new to investing, start with a diversified portfolio inside a stocks and shares ISA.

If you hold a short position when a company goes ex-dividend, the dividend amount is deducted from your account. This is because you have effectively borrowed shares from someone who would have received the dividend. This is an additional cost of shorting dividend-paying stocks.

Related Reading

Explore more investing guides on Smart Investor UK:

- How to Start Investing in the UK - Complete beginner's guide

- How to Buy Shares UK - Step-by-step share buying guide

- Capital Gains Tax on Shares UK - Full guide to CGT rules

- Best Trading Platforms UK - Compare UK investment platforms

- Investing Strategies for Beginners - Proven approaches for UK investors

- How to Invest in the S&P 500 UK - Popular index investing guide

- Stocks and Shares ISA Explained - Tax-free investing basics

- How to Invest in Gold UK - Diversify with precious metals

Smart Investor UK is editorially independent. Some links in this article are affiliate links, meaning we may earn a commission if you open an account, at no extra cost to you. This does not affect our editorial independence or the recommendations we make.

Capital at risk. The value of investments can go down as well as up. You may get back less than you invest. Short selling carries a high risk of loss. Between 70% and 80% of retail CFD accounts lose money. Tax treatment depends on individual circumstances and may change. If you are unsure about investing, seek independent financial advice.