Trading 212 is regulated by the Financial Conduct Authority (FCA) in the UK and holds licences from four other financial regulators worldwide. Your investments are held in segregated accounts, separate from Trading 212's own funds. UK clients are protected by the FSCS up to £85,000 for investments and £120,000 for cash deposits. With over 5 million funded accounts and £25 billion in client assets, Trading 212 is a legitimate and well-established platform.

When you are trusting a platform with your money, the safety question is not just reasonable, it is essential. Trading 212's zero-commission model and slick app can feel too good to be true, and I completely understand why so many people ask whether it is actually safe before depositing their first pound.

I have been using Trading 212 for over a year and have done extensive research into how the platform protects your money. In this guide, I will walk through every layer of protection in plain English: the regulation, the compensation schemes, what happens if Trading 212 goes bust, and the potential risks you should be aware of.

For a full overview of the platform, including fees, features, and my verdict, read my Trading 212 review.

FCA Regulation: What It Means for You

Trading 212 UK Ltd is authorised and regulated by the Financial Conduct Authority (FCA) with firm reference number 609146. You can verify this yourself on the FCA register at register.fca.org.uk.

Being FCA regulated means Trading 212 must meet strict rules on how it handles your money, how it reports to regulators, and how it communicates with customers. The FCA is one of the most respected financial regulators in the world, and any firm that holds an FCA licence is subject to regular oversight and compliance checks.

Beyond the FCA, Trading 212 also holds licences from BaFin (Germany's Federal Financial Supervisory Authority), ASIC (Australian Securities and Investments Commission), CySEC (Cyprus Securities and Exchange Commission), and the FSC (Bulgaria's Financial Supervision Commission). The fact that Trading 212 is regulated by multiple tier-one authorities is a strong trust signal, as many smaller brokers only hold a single licence.

Segregated Accounts: Your Money Is Kept Separate

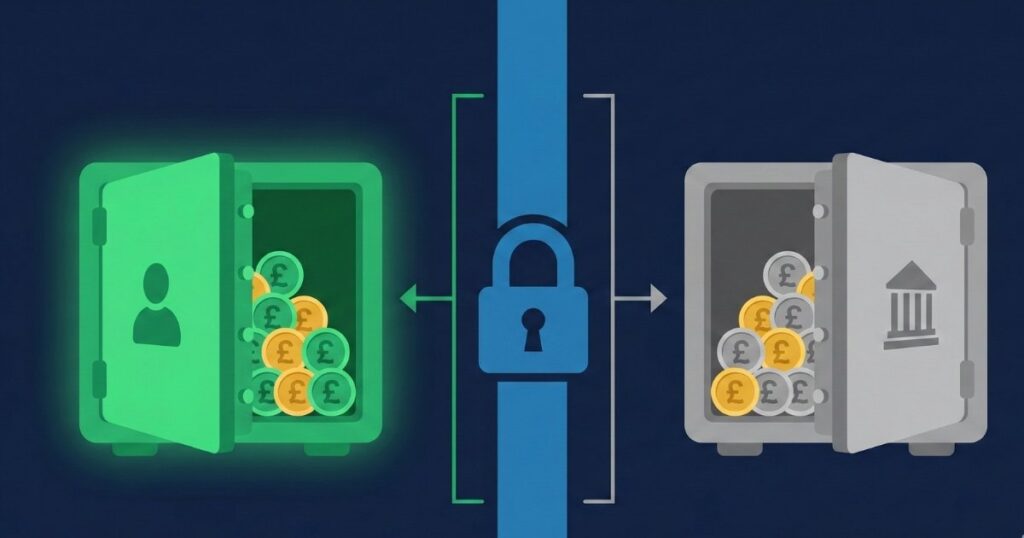

One of the most important protections is that Trading 212 holds your investments and cash in segregated accounts. This means your money is kept completely separate from Trading 212's own operational funds.

Why does this matter? If Trading 212 were to get into financial difficulty or go bust, your assets would not be used to pay off the company's debts. They are ring-fenced and would be returned to you. This is a legal requirement for FCA-regulated firms, and Trading 212 complies with it.

FSCS Protection: How Much Is Covered

UK clients are protected by the Financial Services Compensation Scheme (FSCS), which is the UK's statutory compensation scheme for customers of authorised financial services firms.

For investments (Invest account and Stocks and Shares ISA): FSCS covers up to £85,000 per person. This protection applies if Trading 212 fails and is unable to return your investments. It does not protect you against investment losses due to market movements, which is a normal part of investing.

For cash deposits (Cash ISA): FSCS covers up to £120,000 per person. This increased limit was introduced in December 2025 and applies to eligible cash deposits held with UK-authorised firms. I cover the Cash ISA in detail in my Trading 212 Cash ISA review.

It is worth noting that FSCS protection is per person, per firm. If you hold accounts with multiple providers, each one is protected separately up to the relevant limit.

What Happens If Trading 212 Goes Bust?

This is the question that worries people most, and the answer is reassuring. Because your investments are held in segregated accounts, they would not form part of Trading 212's estate in an insolvency. Your shares and ETFs are held in your name (or in a nominee account on your behalf), and they would be transferred to another broker or returned to you.

If for any reason the segregated assets could not be fully returned, FSCS would step in to cover the shortfall up to the £85,000 limit for investments or £120,000 for cash.

With over 5 million funded accounts and more than £25 billion in client assets, Trading 212 is one of the largest retail brokers in Europe. It has been operating since 2004, which gives it over 20 years of track record. While no investment platform is risk-free, Trading 212 is not a small or untested operator.

How Trading 212 Makes Money

Understanding how a platform makes money helps assess whether its business model is sustainable, which is a legitimate safety concern. Trading 212's revenue comes from several sources:

FX conversion fees. The 0.15% fee charged when you trade assets in a currency different to your account is one of the main revenue streams. On millions of trades, this adds up significantly.

CFD trading. Trading 212 offers a CFD (Contract for Difference) account alongside its Invest and ISA accounts. CFD trading generates revenue through spreads and overnight swap fees. This is a separate product from the commission-free investing side, and it is worth noting that CFDs are high-risk products where the majority of retail investors lose money.

Interest on uninvested cash. Trading 212 earns a margin on the cash held in your account by investing it in qualifying money market funds. They pass most of this interest on to you, but retain a small portion.

Securities lending. If you opt in, Trading 212 can lend your shares to other market participants. You receive a share of the interest earned, and Trading 212 keeps a portion. This is optional and your shares are backed by collateral.

Payment for order flow. In some markets, Trading 212 receives payment from market makers for directing trade orders to them. This is regulated and standard practice across many brokers.

The key takeaway is that Trading 212 has multiple revenue streams that support the zero-commission model. It is not relying on a single income source, which makes the business model more sustainable.

Platform Security

Beyond financial regulation, Trading 212 implements standard security measures to protect your account. Two-factor authentication (2FA) is available and should be enabled on every account. The platform uses encryption to protect data in transit, and biometric login (fingerprint or face recognition) is supported on the mobile app.

Potential Risks to Be Aware Of

While Trading 212 is a safe and regulated platform, there are some risks that are worth understanding:

Investment risk. FSCS and segregated accounts protect you if Trading 212 fails as a company. They do not protect you from investment losses. If the stocks or ETFs you buy fall in value, that is a normal part of investing. My guide on how to start investing in the UK covers how to manage this risk through diversification.

CFD risk. If you use the CFD account, be aware that the majority of retail investors lose money trading CFDs. I would recommend that beginners stick to the Invest or ISA accounts.

Variable interest rates. The Cash ISA rate tracks the Bank of England base rate. If rates fall, your returns will decrease.

No SIPP. Trading 212 does not currently offer a pension product. If pension investing is important to you, you will need a separate provider. My best SIPP UK guide covers the top options.

App-only support. Trading 212 does not offer telephone support. Customer service is handled through the in-app chat, which is generally responsive but may not suit everyone.

How Does Trading 212 Compare on Safety?

All FCA-regulated investing platforms in the UK offer the same core protections: segregated accounts and FSCS coverage. Where Trading 212 differs from traditional brokers like Hargreaves Lansdown or Interactive Investor is that it is a newer, fintech-focused platform without the decades of track record that the established names have.

That said, with over 20 years of operation, 5 million funded accounts, and regulation from five financial authorities, Trading 212 has earned its place among the credible UK brokers. If you are comparing platforms, my best trading platforms UK guide covers how all the main options stack up.

My Verdict: Is Trading 212 Safe?

Yes, Trading 212 is safe to use for investing in the UK. It is FCA regulated, your money is held in segregated accounts, and you are covered by FSCS protection. The platform has been operating for over 20 years and serves millions of customers.

No platform is completely without risk, and the usual caveats about investment risk apply. But from a platform safety perspective, Trading 212 meets every standard you would expect from a reputable UK broker.

If you are ready to get started, my Trading 212 review covers the full platform, and you can claim a free share through my Trading 212 promo code guide.

Frequently Asked Questions

Yes. Trading 212 UK Ltd is authorised and regulated by the Financial Conduct Authority with firm reference number 609146. You can verify this on the FCA register.

Yes. Your investments are held in segregated accounts and would be returned to you. FSCS also covers up to £85,000 for investments and £120,000 for cash deposits.

Yes. Trading 212 was founded in 2004, has over 5 million funded accounts, holds more than £25 billion in client assets, and is regulated by five financial authorities including the FCA.

Yes. Both the Stocks and Shares ISA and Cash ISA are covered by FCA regulation and FSCS protection. The Cash ISA deposits are protected up to £120,000. Read my Trading 212 Stocks and Shares ISA review and Trading 212 Cash ISA review for more details.

Only if you opt in. Securities lending is optional. If you enable it, your shares are backed by collateral and you receive a portion of the interest earned.

Yes. The free share offer is a genuine marketing promotion. You receive a randomly selected fractional share worth between £8 and £100 when you sign up and deposit at least £1. I cover all the details in my Trading 212 promo code guide.