A SIPP gives you tax relief on contributions (20% to 45%) and a higher annual allowance (£60,000), but your money is locked until age 55 (57 from 2028). A stocks and shares ISA has a £20,000 allowance with no tax relief on contributions, but withdrawals are completely tax-free at any time. Most UK investors benefit from using both: ISA first for flexibility, then SIPP for retirement tax relief.

SIPPs and stocks and shares ISAs are the two most popular tax-efficient investment accounts in the UK. Both shelter your investments from income tax and capital gains tax while they grow. But they work in fundamentally different ways, and choosing the right one (or the right balance of both) can make a significant difference to your long-term wealth.

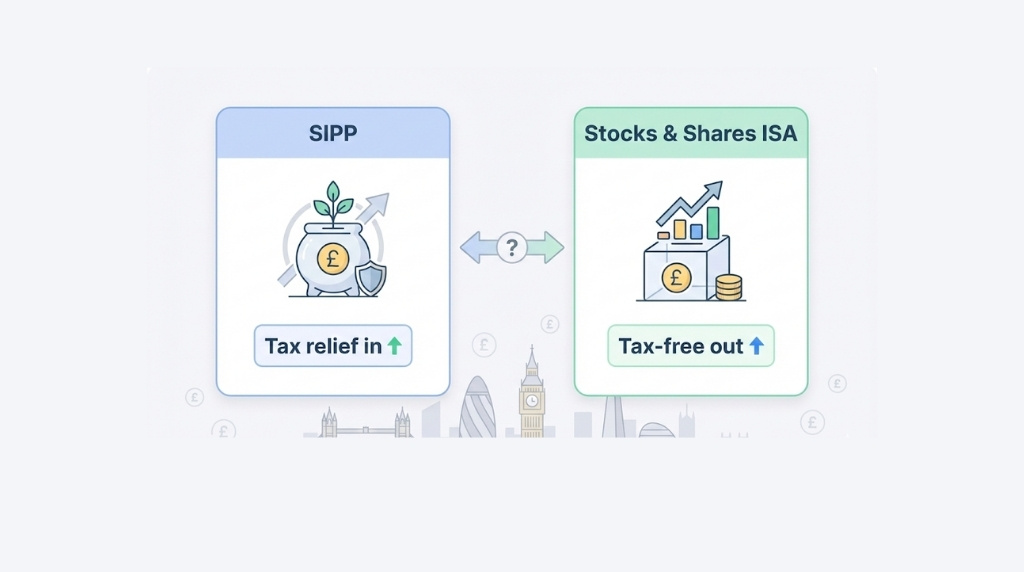

The core difference is simple: a SIPP gives you a tax boost going in but taxes you coming out. An ISA takes already-taxed money but gives you completely tax-free withdrawals. Understanding which approach works best for your situation is one of the most important financial decisions you can make.

What Is a SIPP?

A Self-Invested Personal Pension (SIPP) is a type of personal pension that gives you full control over how your retirement savings are invested. Unlike a standard workplace pension where your employer's provider makes investment decisions, a SIPP lets you choose from a wide range of investments including shares, funds, ETFs, bonds, gilts and investment trusts.

SIPPs sit alongside your workplace pension. You can have both, and many investors use a SIPP to consolidate old workplace pensions into one account with lower fees and better investment choices.

How SIPP Tax Relief Works

When you contribute to a SIPP, the government adds tax relief automatically. For every £80 you pay in, HMRC adds £20, making your total contribution £100. This is basic rate relief at 20% (Source: HMRC, 2025/26).

Higher rate (40%) and additional rate (45%) taxpayers can claim the extra relief through their self-assessment tax return. This means a £100 pension contribution effectively costs a higher rate taxpayer just £60 and an additional rate taxpayer just £55.

The annual allowance for pension contributions is £60,000 for 2025/26, or 100% of your earnings, whichever is lower (Source: GOV.UK, 2025/26). You can carry forward unused allowances from the previous three tax years if you were a member of a registered pension scheme. High earners with adjusted income above £260,000 face a tapered allowance, reducing to a minimum of £10,000.

Accessing Your SIPP

You cannot access your SIPP until age 55, rising to age 57 from 6 April 2028 (Source: GOV.UK, Pension Schemes Act 2021). When you do access it, you can take 25% as a tax-free lump sum. The remaining 75% is taxed as income at your marginal rate when you withdraw it.

What Is a Stocks and Shares ISA?

A stocks and shares ISA is a tax-free wrapper for investments. You contribute money that has already been taxed through your salary, but once inside the ISA, your investments grow completely free from income tax and capital gains tax. When you withdraw, you pay no tax at all.

The annual ISA allowance is £20,000 for 2025/26 (Source: HMRC, 2025/26). This limit covers all ISA types combined: cash ISA, stocks and shares ISA, Lifetime ISA and innovative finance ISA. Unlike the pension allowance, you cannot carry forward unused ISA allowance. If you do not use it by 5 April, it is gone.

Key ISA Benefits

- No tax on dividends, interest or capital gains inside the ISA

- Withdraw your money at any time with no tax or penalties

- No impact on your tax code or benefits

- No need to declare ISA income or gains on your tax return

- ISA savings are not counted as income, so they do not affect means-tested benefits

- A SIPP gives you tax relief going in but taxes you on the way out. An ISA gives no upfront relief but offers completely tax-free withdrawals. Both shelter your investments from tax while they grow.

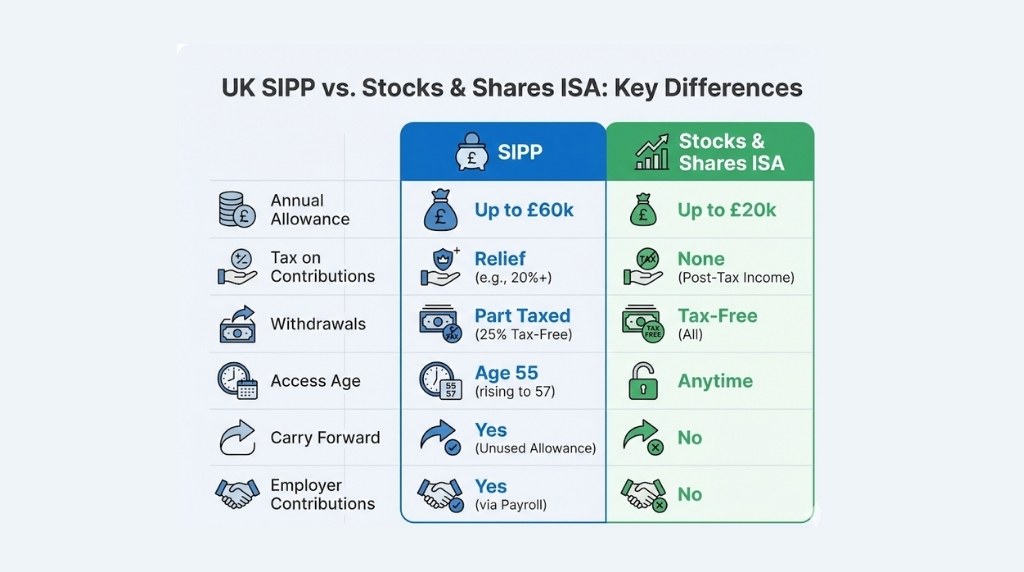

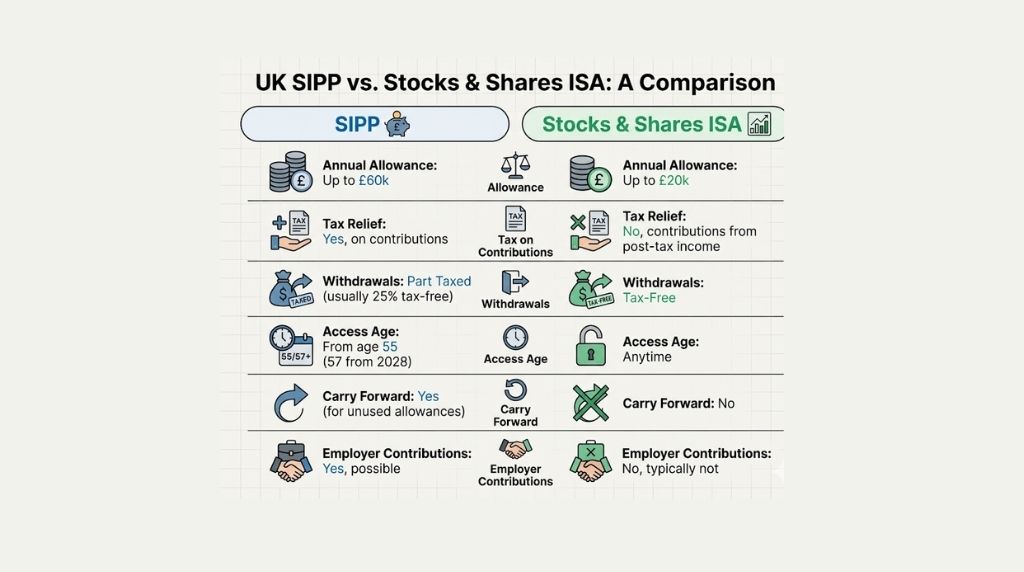

SIPP vs ISA: The Key Differences at a Glance

SIPP vs Stocks and Shares ISA

| Feature | SIPP | Stocks and Shares ISA |

|---|---|---|

| Annual allowance | £60,000 (or 100% of earnings) | £20,000 |

| Tax relief on contributions | 20% to 45% (added by HMRC) | None |

| Tax on growth | Tax-free | Tax-free |

| Tax on withdrawals | 25% tax-free, rest taxed as income | 100% tax-free |

| Access age | 55 (57 from April 2028) | Any time |

| Carry forward unused allowance | Yes (3 previous tax years) | No |

| Employer contributions | Yes (tax-efficient for employers) | No |

| Inheritance tax | Potentially exempt (outside estate) | Part of estate (IHT may apply from April 2027) |

| Impact on benefits | May affect means-tested benefits on withdrawal | No impact |

| Lifetime limit | No lifetime allowance (abolished April 2024) | No lifetime limit |

How Much Tax Relief Do You Actually Get?

The value of pension tax relief depends entirely on your income tax rate. Here is what a £1,000 gross pension contribution actually costs at each tax band.

SIPP Tax Relief Examples (£1,000 Gross Contribution)

| Tax Band | Tax Rate | You Pay | HMRC Adds | Total in SIPP | Effective Boost |

|---|---|---|---|---|---|

| Basic rate | 20% | £800 | £200 | £1,000 | +25% |

| Higher rate | 40% | £600 | £400 | £1,000 | +67% |

| Additional rate | 45% | £550 | £450 | £1,000 | +82% |

| Scottish higher rate | 42% | £580 | £420 | £1,000 | +72% |

For an ISA, every £1,000 you invest costs you exactly £1,000 because there is no tax relief on contributions. The advantage comes later: every penny you withdraw is tax-free.

Worked Example: SIPP vs ISA Over 20 Years

Suppose a higher rate taxpayer invests £500 per month for 20 years, earning 7% annualised returns.

SIPP route: £500 per month after tax relief becomes £833 per month gross (£500/0.6). After 20 years at 7%, the pot grows to approximately £434,000. Taking 25% tax-free (£108,500) and withdrawing the rest at 20% basic rate in retirement leaves approximately £369,000 after tax.

ISA route: £500 per month (no top-up). After 20 years at 7%, the pot grows to approximately £260,000. All withdrawals are tax-free, so you keep the full £260,000.

In this example, the SIPP produces approximately £109,000 more, largely because of the upfront tax relief allowing more money to be invested and compounded over 20 years.

- The higher your tax rate, the more powerful SIPP tax relief becomes. A higher rate taxpayer effectively gets a 67% government boost on every contribution. However, remember that SIPP withdrawals (beyond the 25% tax-free lump sum) are taxed as income.

When Should You Choose a SIPP?

A SIPP is likely the better choice if:

You are a higher or additional rate taxpayer. The tax relief at 40% or 45% is significantly more valuable than any ISA benefit. If you pay higher rate tax now but expect to be a basic rate taxpayer in retirement, you benefit twice: relief at 40% going in and only 20% tax coming out.

You want to consolidate old pensions. If you have several workplace pensions from previous employers, transferring them into a single SIPP can reduce fees, simplify management and give you better investment options. See our best SIPP provider comparison.

Your employer offers matched contributions. Employer pension contributions are not subject to income tax or National Insurance, making them one of the most tax-efficient forms of compensation. Always take full advantage of employer matching before considering an ISA.

You have already used your ISA allowance. With a £20,000 ISA cap, higher earners often fill their ISA and still have money to invest. The SIPP's £60,000 allowance (plus carry forward) provides additional tax-efficient capacity.

You want inheritance tax benefits. Pension pots are currently exempt from inheritance tax and sit outside your estate. SIPPs can be passed to beneficiaries tax-free if you die before 75, or taxed at the beneficiary's marginal rate if after 75. Note: the government has announced that pensions will be brought within IHT from April 2027 (Source: GOV.UK, Autumn Budget 2025).

When Should You Choose a Stocks and Shares ISA?

An ISA is likely the better choice if:

You need access before retirement age. ISA money is available at any time with no penalties or tax. If you are saving for a house deposit, career break, or simply want financial flexibility, an ISA is essential.

You are a basic rate taxpayer. At 20% tax relief, the SIPP advantage is smaller. If you are also likely to be a basic rate taxpayer in retirement, the net benefit of the SIPP over an ISA is modest. The ISA's flexibility may outweigh the pension's tax advantage.

You are close to or above the pension taper threshold. If your adjusted income exceeds £260,000, your pension annual allowance reduces. The ISA allowance is unaffected by income level.

You want to avoid tax on withdrawals entirely. ISA withdrawals have no impact on your tax code, state pension calculations, means-tested benefits or student loan repayments. SIPP withdrawals count as income and can affect all of these.

You are under 18. Junior ISAs allow up to £9,000 per year in tax-free investments, accessible at age 18. Junior SIPPs have a £2,880 net allowance and funds are locked until retirement.

Can You Have Both a SIPP and an ISA?

Yes, and most financial planners recommend it. A SIPP and an ISA are completely separate allowances. You can contribute £60,000 to a SIPP and £20,000 to an ISA in the same tax year, sheltering up to £80,000 from tax.

A common strategy for UK investors is:

- Step 1: Maximise employer pension matching (free money).

- Step 2: Fill your stocks and shares ISA (£20,000) for flexible, tax-free savings.

- Step 3: Top up your SIPP with additional contributions, especially if you are a higher rate taxpayer.

- Step 4: Use a General Investment Account (GIA) only after both ISA and SIPP allowances are used.

This approach gives you tax-free access to your ISA for medium-term goals and tax-relieved growth in your SIPP for retirement. The combination is far more powerful than either account alone.

Key Takeaway: You do not have to choose between a SIPP and an ISA. Using both maximises your tax efficiency: the ISA for flexibility and the SIPP for retirement tax relief. Prioritise employer pension matching first, then ISA, then additional SIPP contributions.

Best Platforms for SIPPs and ISAs

Many platforms offer both SIPP and ISA accounts, making it easy to manage everything in one place.

Platform Fees: ISA vs SIPP (Quick Comparison)

| Platform | ISA Fee | SIPP Fee | Fund Range | Best For |

|---|---|---|---|---|

| Vanguard | 0.15% (capped £375/yr) | 0.15% (capped £375/yr) | Vanguard funds only | Low-cost index investing |

| InvestEngine | 0% (DIY ETFs) | 0.15% | ETFs only | Fee-free ISA investing |

| Hargreaves Lansdown | 0.45% (capped) | 0.45% (capped) | Widest range | Largest fund choice |

| Interactive Investor | From £4.99/mo | From £4.99/mo | Wide range | Flat-fee for larger pots |

| Trading 212 | 0% (stocks & ETFs) | N/A (no SIPP) | 4,500+ shares, ETFs | Commission-free ISA |

See our full best trading platforms UK guide and best SIPP provider UK comparison for detailed reviews.

Frequently Asked Questions

It depends on your circumstances. A SIPP is better for retirement saving, especially for higher rate taxpayers who get 40% or 45% tax relief. An ISA is better for flexibility and goals you want to access before retirement. Most investors benefit from having both.

Not directly. ISAs and SIPPs are separate tax wrappers with different rules. You can withdraw money from an ISA and contribute it to a SIPP, but you would lose the ISA tax-free wrapper on that money. The contribution to the SIPP would count towards your pension annual allowance.

Only after you reach the minimum pension access age (currently 55, rising to 57 from April 2028). At that point, you can withdraw from your SIPP and contribute to an ISA, subject to the £20,000 annual ISA allowance. Note that SIPP withdrawals beyond the 25% tax-free lump sum are taxed as income.

Currently, SIPPs sit outside your estate for inheritance tax purposes. If you die before 75, your beneficiaries receive the pension tax-free. After 75, they pay income tax at their marginal rate on withdrawals. From April 2027, pensions may be brought within IHT (Source: GOV.UK, Autumn Budget 2025).

ISAs form part of your estate for inheritance tax purposes. However, your spouse or civil partner can inherit your ISA allowance as an Additional Permitted Subscription (APS), effectively allowing them to reinvest the value of your ISA tax-free.

Fill your employer pension match first (it is free money). Then most advisers recommend filling your ISA for flexibility, followed by additional SIPP contributions for tax relief. Higher rate taxpayers may prioritise the SIPP due to the more generous tax relief.

The standard pension annual allowance is £60,000 or 100% of your earnings, whichever is lower. This covers all pension contributions including employer, personal and SIPP. Unused allowance from the previous three tax years can be carried forward (Source: HMRC, 2025/26).

Yes, there is no limit on the number of SIPPs you can hold. However, your total contributions across all pensions must not exceed the annual allowance. Having multiple SIPPs may also mean paying multiple sets of fees.

Currently age 55. This rises to age 57 from 6 April 2028 under the Pension Schemes Act 2021. Some older pension schemes may have a protected pension age of 55, but this depends on when the scheme was set up.

No. ISA withdrawals are not counted as income and have no effect on your state pension, tax code, or means-tested benefits. This is one of the key advantages of ISA savings in retirement compared to SIPP withdrawals, which are taxed as income.

Related Reading

Explore more investing guides on Smart Investor UK:

- What Is a SIPP? - Complete guide to self-invested personal pensions

- Best SIPP Provider UK - Compare the top SIPP accounts

- Stocks and Shares ISA Explained - How ISAs work

- Best Stocks and Shares ISA - Compare ISA platforms

- SIPP Tax Relief Explained - How pension tax relief works

- Lifetime ISA Rules - LISA vs SIPP for retirement

- Capital Gains Tax on Shares UK - CGT rules for investors

- How to Start Investing in the UK - Complete beginner's guide

Smart Investor UK is editorially independent. Some links in this article are affiliate links, meaning we may earn a commission if you open an account, at no extra cost to you. This does not affect our editorial independence or the recommendations we make.

Capital at risk. The value of investments can go down as well as up. You may get back less than you invest. Tax treatment depends on individual circumstances and may change. Pension and ISA rules may be subject to change. If you are unsure about investing, seek independent financial advice.