A stocks and shares ISA is a tax-free investment account that lets UK residents invest up to £20,000 per year in funds, shares, bonds, and ETFs without paying capital gains tax or dividend tax on returns. The average stocks and shares ISA has returned 9.64% annually over the past decade (Finder/Moneyfacts, 2025), compared to just 1.2% for cash ISAs over the same period. You must be 18 or over and a UK resident to open one.

What Is a Stocks and Shares ISA?

A stocks and shares ISA (also called an investment ISA) is a tax-efficient wrapper that lets you invest in the stock market without paying UK tax on your returns. Any capital gains, dividends, or interest you earn inside the ISA are completely free from income tax, capital gains tax, and dividend tax.

The "ISA" stands for Individual Savings Account, a government scheme introduced in 1999 to encourage saving and investing. While a cash ISA works like a standard savings account that pays tax-free interest, a stocks and shares ISA lets you hold a far wider range of assets, including company shares, investment funds, exchange-traded funds (ETFs), bonds, and investment trusts.

According to HMRC data analysed by AJ Bell (September 2025), there is now over £511 billion invested in stocks and shares ISAs across the UK, more than doubling from £241 billion in 2014. Despite this growth, only around 15% of UK adults currently hold a stocks and shares ISA (Finder, January 2025), suggesting many people are missing out on one of the simplest ways to invest tax-free.

Key Takeaway — What Makes It Different:

Unlike a cash ISA, a stocks and shares ISA gives your money the potential to grow by investing in the stock market. Returns are not guaranteed and your capital is at risk, but historically, investment ISAs have significantly outperformed cash savings over the medium to long term.

How Does a Stocks and Shares ISA Work?

A stocks and shares ISA works by placing a tax-free "wrapper" around your investments. You open an account with a platform or provider, deposit money (up to your annual ISA allowance), and then choose where to invest that money within the account.

Here is how the process works step by step:

1. Open an account. Choose an investment platform that offers a stocks and shares ISA. You will need to be 18 or over and a UK resident for tax purposes. Most providers let you open an account online in minutes.

2. Deposit money. Add funds up to your annual ISA allowance of £20,000 for the 2025/26 tax year. You can deposit a lump sum, set up a monthly direct debit, or both.

3. Choose your investments. Select from a range of assets including index funds, ETFs, individual shares, bonds, and investment trusts. Many platforms also offer ready-made portfolios.

4. Your investments grow tax-free. Any gains, dividends, or interest earned within your ISA are sheltered from UK tax. You do not need to declare ISA returns on your tax return.

5. Withdraw at any time. Unlike a pension, you can access your money whenever you need it. However, withdrawing does reduce your ISA allowance for that tax year unless your provider offers a "flexible" ISA.

The tax wrapper stays in place for as long as you hold the ISA. There is no time limit and no requirement to withdraw at a certain age. Money that stays invested continues to grow tax-free indefinitely.

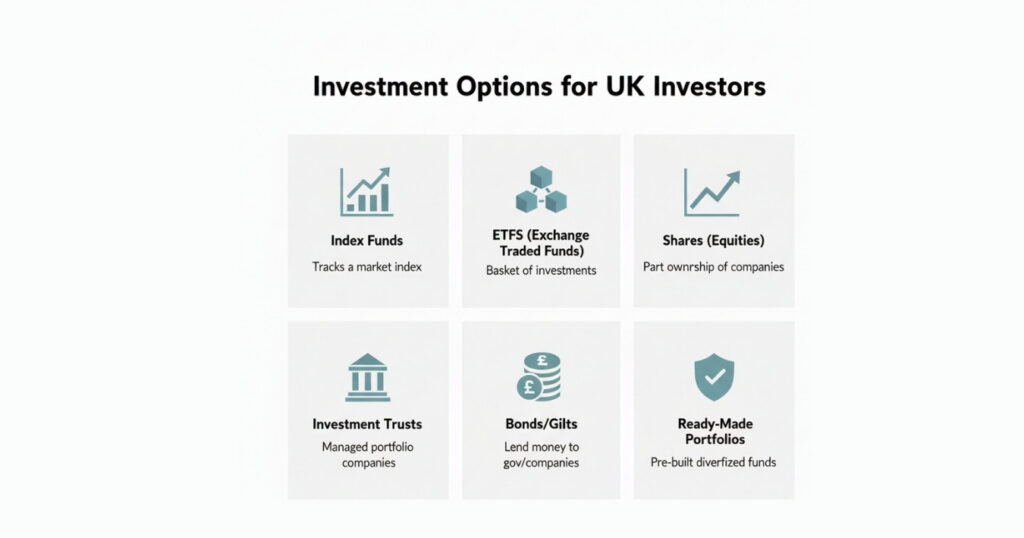

What Can You Hold in a Stocks and Shares ISA?

A stocks and shares ISA can hold a wide range of investments. The most common options include:

Types of Investments in a Stocks and Shares ISA

| Investment Type | What It Is | Risk Level | Best For |

|---|---|---|---|

| Index funds | Funds tracking a market index (e.g. FTSE 100, S&P 500) | Medium | Beginners, long-term growth |

| ETFs | Similar to index funds but traded on a stock exchange | Medium | Cost-conscious investors |

| Individual shares | Direct ownership of company stock | Higher | Experienced investors |

| Investment trusts | Publicly listed professionally managed funds | Medium-High | Income and growth seekers |

| Bonds and gilts | Government or corporate debt instruments | Lower | Capital preservation |

| Ready-made portfolios | Pre-built diversified portfolios matched to risk | Varies | Hands-off investors |

If you are new to investing, starting with a low-cost global index fund or a ready-made portfolio is the simplest approach. For more guidance, see our article on how to start investing in the UK.

Stocks and Shares ISA Rules for 2025/26

Understanding the current rules will help you make the most of your ISA. Here are the key rules for the 2025/26 tax year (6 April 2025 to 5 April 2026):

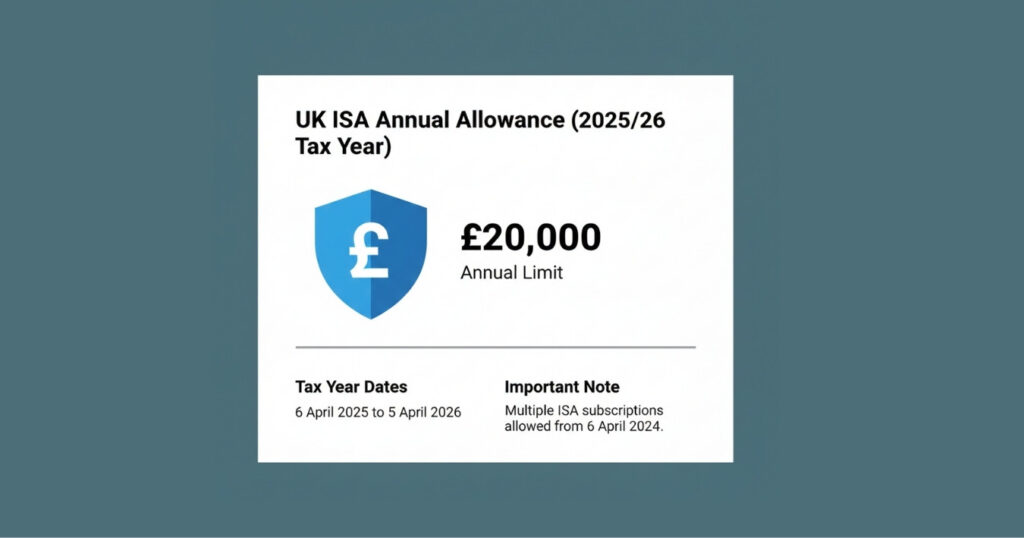

Annual Allowance

The stocks and shares ISA allowance for 2025/26 is £20,000. This is the maximum you can deposit across all your ISAs in a single tax year. You can split the £20,000 between a stocks and shares ISA, a cash ISA, an innovative finance ISA, and a Lifetime ISA (up to £4,000 of the total), but the combined contributions cannot exceed £20,000.

The ISA allowance has been frozen at £20,000 since the 2017/18 tax year and will remain at this level until at least 2030, following the Autumn Budget 2024 announcement.

Key ISA Rules at a Glance

Stocks and Shares ISA Rules (2025/26)

| Rule | Detail |

|---|---|

| Annual allowance | £20,000 (2025/26) |

| Minimum age | 18 (16 for cash ISAs only) |

| Residency requirement | UK tax resident |

| Multiple ISAs per type | Yes, since 6 April 2024 |

| Use it or lose it | Unused allowance does not roll over |

| Tax on returns | None (no CGT, income tax, or dividend tax) |

| Withdrawals | Allowed at any time (check if flexible ISA) |

| Transfers | Allowed between providers without losing tax-free status |

| Inheritance | ISA benefits pass to spouse/civil partner via APS |

| Junior ISA allowance | £9,000 (separate from adult allowance) |

Rule Change: Multiple ISAs (Since April 2024)

Since 6 April 2024, you can open and contribute to multiple stocks and shares ISAs in the same tax year with different providers. Previously, you could only pay into one stocks and shares ISA per tax year. This change gives investors more flexibility to use specialist platforms for different types of investments while staying within the overall £20,000 limit.

What Are the Tax Benefits of a Stocks and Shares ISA?

The tax advantages of a stocks and shares ISA are substantial, especially as the government has reduced personal tax allowances in recent years. Here is what you do not pay inside an ISA:

Capital gains tax (CGT): Outside an ISA, gains above £3,000 per year (2025/26) are taxed at 18% for basic rate or 24% for higher rate taxpayers. The CGT allowance was £12,300 as recently as 2022/23, making ISAs significantly more valuable now.

Outside an ISA, dividends above £1,000 per year (2025/26) are taxed at 8.75% (basic), 33.75% (higher), or 39.35% (additional rate). The dividend allowance was £2,000 in 2022/23.

Income tax on interest: Any interest from bonds or cash held within your ISA is free from income tax.

No tax return required: You do not need to declare ISA income or gains to HMRC.

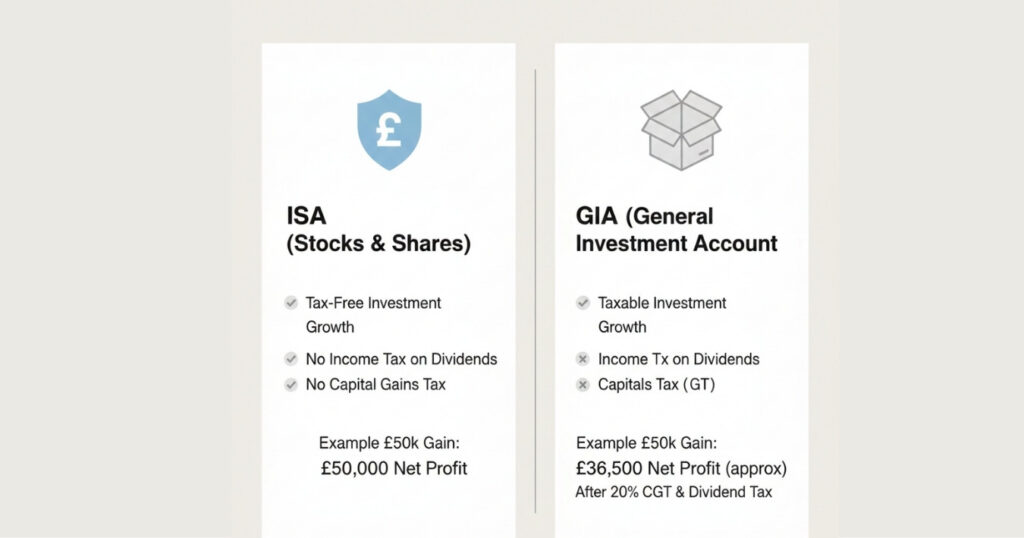

How Much Tax Could You Save?

Consider a £50,000 portfolio earning 8% annually:

Tax Impact: Stocks and Shares ISA vs General Investment Account

| Tax Scenario | Stocks and Shares ISA | General Investment Account |

|---|---|---|

| Annual growth (8%) | £4,000 | £4,000 |

| Capital gains tax | £0 | Up to £240 (after £3k allowance) |

| Dividends (est. £1,000) | £0 tax | Up to £87.50 (basic rate) |

| After 20 years | £233,048 | £209,000–£218,000 |

| Tax saved over 20 years | — | £15,000–£24,000 |

The tax savings compound over time. As the Barclays Equity Gilt Study (2024) found, shares have outperformed cash nine times out of ten over any ten-year period during the past 130 years.

- With the CGT allowance reduced to £3,000 and the dividend allowance cut to £1,000, the Stocks and Shares ISA has become one of the most important tax shelters for UK investors.

Stocks and Shares ISA vs Cash ISA: Which Should You Choose?

This is one of the most common questions for UK savers. The short answer: it depends on your time horizon and goals.

Stocks and Shares ISA vs Cash ISA Comparison

| Factor | Stocks and Shares ISA | Cash ISA |

|---|---|---|

| 10-year annual return | 9.64% | 1.2% |

| Risk to capital | Yes — value can fall | No — capital protected |

| Best for | Medium to long term (5+ yrs) | Short term / emergency funds |

| Beat inflation? | Historically yes, over 5+ yrs | Rarely |

| FSCS protection | Up to £85,000 per provider | Up to £85,000 per provider |

| Min recommended period | 5 years | No minimum |

According to Moneyfactscompare.co.uk (February 2025), the average stocks and shares ISA fund returned 11.86% in the year to February 2025, compared to 3.80% for the average cash ISA. Over ten years, investment ISAs have returned roughly eight times more than their cash equivalents.

However, cash ISAs are not without merit. They beat stocks and shares ISAs in two consecutive years (2022 and 2023) when markets fell while savings rates rose. For money you need within one to three years, a cash ISA or savings account is generally safer.

A sensible approach is to hold both: a cash ISA or emergency fund for short-term needs, and a stocks and shares ISA for medium to long-term wealth building. For a detailed comparison, see our guide to cash ISA vs stocks and shares IS.

How to Open a Stocks and Shares ISA

Opening a stocks and shares ISA takes just a few minutes. Here is what you need to do:

Step 1: Choose a platform.

Compare investment platforms based on fees, investment range, and ease of use. For our top picks, see best stocks and shares IS.

Step 2: Check eligibility.

You must be 18 or over, a UK tax resident, and have not exceeded your £20,000 ISA allowance for the current tax year.

Step 3: Open the account.

Provide your personal details, National Insurance number, and bank account information.

Step 4: Fund your ISA.

Transfer money via bank transfer or set up a direct debit. Many platforms allow you to start with as little as £1 for lump sums or £25 per month.

Step 5: Choose your investments.

Select funds, shares, ETFs, or a ready-made portfolio. A global index fund tracking the FTSE All-World gives instant diversification across thousands of companies.

Step 6: Review regularly.

Check periodically but avoid reacting to short-term movements. According to Capital Group, 90% or more of active fund managers fail to beat their benchmark over 15 years, which is why low-cost index funds are the default recommendation.

What Returns Can You Expect from a Stocks and Shares ISA?

Returns depend entirely on what you invest in. There is no fixed rate and your capital is at risk. History provides useful context:

Historical Investment Benchmarks

| Benchmark | Annual Return | Period | Source |

|---|---|---|---|

| Avg S&S ISA fund | 9.64% | 10 yrs to 2024 | Finder/Moneyfacts |

| FTSE 100 total return | 7.48% | 1984–2022 | Investing in the Web |

| S&P 500 total return | 10.3% | 1957–2022 | S&P Global |

| Global equities (real) | 5.2% | 125 years | UBS/Cambridge 2025 |

| Average cash ISA | 1.2% | 10 yrs to 2024 | Finder/Moneyfacts |

Sources: Finder/Moneyfacts, Investing in the Web, S&P Global, UBS/Cambridge 2025. Past performance is not a reliable indicator of future results.

The Barclays Equity Gilt Study (2024) found that over any ten-year period during the past 130 years, shares outperformed cash nine times out of ten. This is why professionals recommend investing for a minimum of five years. To project your own returns, try our investment calculator.

- Short-term market drops are normal and expected. Over five-year periods and beyond, the historical probability of positive returns from a diversified equity portfolio has been strongly in investors’ favour. Staying invested allows compounding to do the heavy lifting.

Common Mistakes to Avoid with a Stocks and Shares ISA

Not using your full allowance. If you can afford to, use as much of your £20,000 as possible each year. Unused allowance cannot be carried forward, and it is frozen until 2030.

Leaving money in cash within the ISA. Depositing money but not investing it is surprisingly common. Cash sitting in an investment ISA typically earns little or no interest.

Chasing past performance. Last year's top fund will not necessarily perform well this year. Stick to a diversified, low-cost strategy.

Paying high fees. A 2% annual fee costs roughly £71,500 more than a 0.1% fee over 30 years on a £200/month investment at 7% growth.

Panic selling during downturns. Markets fall regularly but have always recovered historically. Selling during a dip locks in losses.

Forgetting to transfer old ISAs. If you have ISAs with high-fee providers, transfer to a cheaper platform using the formal ISA transfer process.

Frequently Asked Questions

For most people investing for five or more years, yes. The tax-free growth becomes increasingly valuable as your portfolio grows. However, your capital is at risk and returns are not guaranteed.

Yes. Your money is invested in financial markets and its value can fall as well as rise. A minimum five-year investment horizon is generally recommended.

Invest as much as you can afford after building an emergency fund covering three to six months of expenses. Even £50 or £100 per month can grow significantly over the long term.

Yes. You can hold both in the same tax year, and combined contributions must not exceed the £20,000 annual ISA allowance.

The ISA loses its tax-free status on death, but a spouse or civil partner receives an Additional Permitted Subscription equal to the ISA’s value. ISAs may form part of your estate for inheritance tax purposes.

The ISA deadline for the 2025/26 tax year is 5 April 2026. Any unused allowance is lost after this date.

No. Withdrawals are tax-free. However, withdrawing reduces your available contribution room for that tax year unless you have a flexible ISA.

A SIPP provides tax relief on contributions but locks money away until at least age 57. A stocks and shares ISA offers no upfront tax relief but allows access to funds at any time.

Yes. Use the formal ISA transfer process through your new provider. Do not withdraw and redeposit funds, as this would use your annual allowance.

Investments are not protected against market losses. However, if your platform fails, the FSCS protects up to £85,000 per person per firm. Investments are held separately from the platform’s own assets.

Related Reading

Best Stocks and Shares ISA — Our top-rated platforms for 2026

Cash ISA vs Stocks and Shares ISA — A detailed comparison

How to Start Investing in the UK — Complete beginner's guide

ISA Allowance 2025/26 — Everything about ISA limits

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Investing in a stocks and shares ISA involves risk; the value of your investments can go down as well as up, and you may get back less than you invest. Tax rules depend on individual circumstances and may change. Always consider your own financial situation before investing and seek independent financial advice if needed.