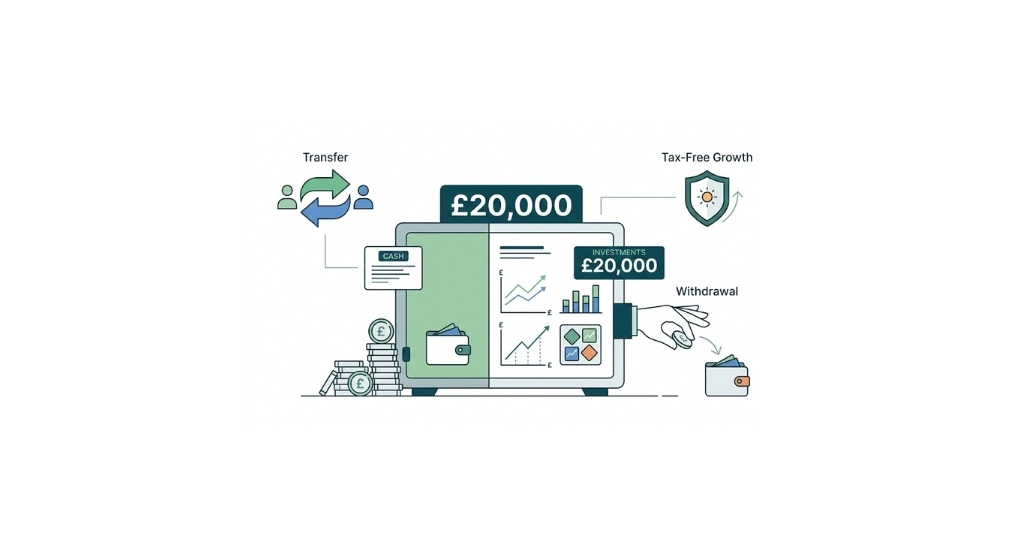

A Stocks and Shares ISA is a UK investment account that protects your returns from UK tax. You can invest up to £20,000 total across ISAs in the 2025/26 tax year (6 April 2025 to 5 April 2026). Since April 2024, the rules also became more flexible: you can typically contribute to more than one ISA of the same type in the same tax year (Lifetime ISAs are the main exception).

The big “don’t mess this up” rule is transfers: always transfer using the new provider’s ISA transfer process, not by withdrawing to your bank and paying it back in yourself. If you withdraw and re-deposit the wrong way, you can accidentally use up your allowance or lose tax-free status.

Also, ISA rules are changing fast. A niche but important example: cryptoasset exchange-traded notes (cETNs) were allowed for a short period, but new purchases won’t be allowed inside Stocks and Shares ISAs from 6 April 2026 (they move into Innovative Finance ISA rules).

Personal note: I wrote most of this with my six dogs, Charlie, Buster, Ember, Simba, Max and Molly, taking turns to “supervise” the keyboard. It’s a good reminder that ISA rules reward calm, consistent habits, not frantic last-minute decisions.

Rules that matter in real life

The UK’s ISA rules are written to be simple for investors, but the details that catch people out are very specific. Here are the ones I think are genuinely worth knowing before you open, fund, or transfer an ISA.

A Stocks and Shares ISA is designed to let you invest without paying UK tax on income and gains inside the wrapper. In practice, that means you do not need to report ISA income or gains on your tax return, and capital losses inside an ISA do not count for Capital Gains Tax purposes.

The annual ISA subscription limit (across ISAs) is £20,000 for 2025/26. The tax year runs from 6 April to 5 April, and unused allowance does not roll over.

Eligibility is tighter than most people realise. Since 6 April 2024, you generally need to be 18 or over to subscribe to any ISA type, with transitional arrangements for some 16–17 year olds who already had (or were eligible to open) a Cash ISA before the cut-off. Those transitional rules end at 11:59pm on 5 April 2026. If you’re under 18 and investing for a child, a Junior ISA sits under different rules and a different allowance.

Residence matters too. You normally must be UK-resident (or meet specific exceptions such as certain Crown employee situations) to subscribe, and if you become non-resident you can usually keep the ISA but stop adding new money until you qualify again.

If you want a straightforward walkthrough,

see What Is a Stocks and Shares ISA? and How to Open a Stocks and Shares ISA

Subscriptions, multiple accounts, and the allowance trap

Most “ISA mistakes” are not investing mistakes. They are admin mistakes.

You can split your £20,000 allowance across ISA types and accounts. A Lifetime ISA has its own £4,000 limit that sits within the overall £20,000, not on top of it.

A rule change that is still not widely understood: since April 2024, you can generally pay into more than one ISA of the same type in the same tax year (the notable exception is the Lifetime ISA). This is helpful, but it increases the risk that you lose track of contributions across providers. HMRC is clear that if you use multiple managers, it’s your responsibility to stay within the overall limit.

This is where my own process is brutally boring, but effective. I keep a single note on my phone with every ISA deposit listed by date and provider, and once a month I total it. It takes two minutes. It saves a world of pain in March and early April when you’re busy living life, or trying to stop Max from sprinting off with your socks.

If you want the cleanest explanation of how the allowance works, use Isa allowance. If you’re weighing tax wrappers, compare Cash ISA vs Stocks and Shares ISA and sipp vs isa.

What you can hold in a Stocks and Shares ISA

A Stocks and Shares ISA is not a free-for-all. Eligible investments are defined in regulation and HMRC guidance, and providers also apply their own product limits.

At a practical level, most UK platforms let you hold mainstream listed investments such as shares admitted to trading on recognised exchanges, funds (including ETFs and investment trusts), and bonds and gilts.

Two modern rule updates are worth calling out:

Fractional shares are now explicitly supported under updated rules, which matters if you invest small monthly amounts in higher-priced shares.

Cryptoasset ETNs (cETNs) are a moving target. HMRC published a policy position that any cETNs held in Stocks and Shares ISAs before 6 April 2026 would be treated as qualifying Innovative Finance ISA investments from that date, and new purchases in a Stocks and Shares ISA won’t be permitted after 5 April 2026. If you were never planning to buy crypto ETNs, you can ignore this. If you were, you cannot treat “ISA eligibility” as a permanent feature. Rules can and do change.

If you want help choosing a simple long-term portfolio (without turning it into a finance degree),

See our guides to the best ETFs in the UK, best index funds in the UK, best Vanguard funds, and investing strategies for beginners.

Withdrawals, flexible ISAs, and transfers

Withdrawals from an ISA are usually simple: you can take money out when you want. The question is whether you can put it back without using more of your allowance.

If your ISA is “flexible”, money you withdraw in the same tax year can generally be replaced without reducing your remaining allowance, as long as you follow the provider’s flexible ISA rules. GOV.UK provides a straightforward worked example showing how the allowance differs between flexible and non-flexible ISAs after a withdrawal. Not all Stocks and Shares ISAs are flexible, and flexible replacement normally has to go back into the same account it came from.

Transfers are where people accidentally break things. The core rule is simple: you have the legal right to transfer whenever you want, but you must do it via the ISA transfer process with the new manager. If you close the ISA and pay the proceeds into a new ISA yourself, it is treated as a withdrawal and you risk losing the wrapper or using up allowance.

Also, the transfer rules have become more flexible. HMRC’s guidance for managers explicitly discusses partial transfers, including partial transfers involving current-year subscriptions. That matters because a lot of older bank help pages still repeat the pre-2024 type rule of “current year must be transferred in full”. If you’re transferring now, treat HMRC guidance and your provider’s current terms as the source of truth.

If you’re planning to switch provider, read how to transfer a Stocks and Shares ISA. If you’re deciding where to hold your ISA, start with the best Stocks and Shares ISAs, then compare costs and usability via the best trading platforms in the UK and the best trading apps in the UK.

Common mistakes and future changes

Most mistakes come from rushing, especially around tax-year end.

The classic errors are oversubscribing across multiple providers, withdrawing to your bank account and re-depositing instead of transferring, and assuming anything listed on a platform is ISA-eligible forever. If you want a sanity-check on whether investing in an ISA is even right for your timeframe and nerves, use is-stocks-and-shares-isa-worth-it.

Inheritance is another area people miss. If an ISA holder dies, HMRC describes how the ISA can become a continuing account of a deceased investor for up to three years (or until estate administration completes or the account is closed), and income and gains in that continuing account remain tax-advantaged during that period. Separately, a surviving spouse or civil partner may be eligible for an additional ISA allowance linked to the deceased’s ISA value. GOV.UK explains the basic idea for consumers.

Looking ahead, the biggest planned ISA reform is scheduled for 6 April 2027 (so it does not affect what you can subscribe in 2025/26, but it should influence long-term planning). HMRC’s Tax-free Savings Newsletter 19 states that the government plans to introduce a £12,000 Cash ISA subscription limit for under-65s, keep £20,000 for 65+, and add anti-circumvention rules including a ban on transfers from Stocks and Shares ISAs to Cash ISAs for under-65s, “cash-like” investment tests, and a charge on interest paid on cash held in Stocks and Shares ISAs or Innovative Finance ISAs. This is significant, and it’s exactly why I tell readers not to build a plan that relies on today’s ISA mechanics staying unchanged for the next decade. Change is now part of the ISA landscape.

If your next step is choosing a provider, you’ll likely want a mix of independent comparisons and hands-on reviews. These are useful starting points: Trading 212 review, Vanguard review, Freetrade review, Hargreaves Lansdown review, Interactive Investor review, AJ Bell review, and InvestEngine review..

FAQ

What is the Stocks and Shares ISA allowance for 2025/26?

The overall ISA subscription limit for the 2025/26 tax year is £20,000. You can use that allowance across different ISAs, but it’s your job to ensure you stay within the total if you use multiple providers.

Can I have more than one Stocks and Shares ISA?

Yes. You can hold multiple Stocks and Shares ISAs, and since rule changes in April 2024 you can generally contribute to more than one Stocks and Shares ISA in the same tax year, provided you stay within the overall ISA limit. For the fuller explanation (and edge cases).

Can I withdraw from a Stocks and Shares ISA and pay it back in later?

You can withdraw whenever you like, but paying it back without affecting your allowance depends on whether your ISA is “flexible” and whether you replace the money within the same tax year under your provider’s rules.

How do I transfer a Stocks and Shares ISA without losing tax-free status?

Start the transfer through the new provider using an official ISA transfer request. Do not withdraw to your bank and re-deposit, as that can break the wrapper and/or use your allowance. [4] A practical walkthrough is in Transfer-stocks-and-shares-isa.

What investments are not allowed in a Stocks and Shares ISA?

Eligibility is defined by regulation and HMRC guidance, and will vary by provider. One timely example: cryptoasset ETNs have specific transitional treatment and won’t be available for new purchases inside a Stocks and Shares ISA from 6 April 2026.

Do I need to report Stocks and Shares ISA gains to HMRC?

Generally, no. HMRC states investors do not have to declare ISA income or gains on tax returns (unless an ISA is voided), and capital losses in an ISA are disregarded for Capital Gains Tax. For the practical implications, see Stocks-and-shares-isa-tax.

Call to action and author sign-off

If you want to act on this today, keep it simple: pick one good provider, automate a monthly contribution, and track your total subscriptions so you never accidentally drift over the £20,000 limit.

Start here: best Stocks and Shares ISA. If you’re choosing between app-first brokers and more traditional platforms, use best trading apps in the UK and best trading platforms in the UK, then drill into the reviews that match your style of investing.