A SIPP (Self-Invested Personal Pension) is a DIY pension that gives you full control over how your retirement savings are invested. You choose from shares, funds, ETFs, bonds and investment trusts. Contributions receive tax relief at 20% to 45%, with an annual allowance of £60,000 for 2025/26. You cannot access your SIPP until age 55 (rising to 57 from April 2028), at which point you can take 25% tax-free and draw income from the rest.

If you have ever looked at your workplace pension statement and wondered why you have so little control over where your money is invested, a SIPP might be the answer. A Self-Invested Personal Pension puts you in charge of your retirement savings, giving you the freedom to choose your own investments while still benefiting from generous tax relief.

SIPPs have become one of the most popular pension types in the UK, particularly among self-employed workers, people consolidating old workplace pensions, and investors who want more choice than a standard personal pension offers. This guide explains exactly how SIPPs work, who they suit, and how to get started.

What Is a SIPP?

SIPP stands for Self-Invested Personal Pension. It is a type of personal pension registered with HMRC that lets you choose and manage your own investments. Unlike a workplace pension where your employer's provider picks the funds, a SIPP gives you access to a much wider range of investment options.

A SIPP works as a tax-efficient wrapper around your investments. The money you contribute receives tax relief from the government, and your investments grow free from income tax and capital gains tax while inside the pension. When you eventually withdraw, you can take 25% tax-free, with the rest taxed as income (Source: HMRC, 2025/26).

SIPPs were first introduced in the UK in 1990 and have grown significantly in popularity since pension freedoms were introduced in April 2015, which gave savers much greater flexibility in how they access their pension pots (Source: GOV.UK, Pension Freedoms, 2015).

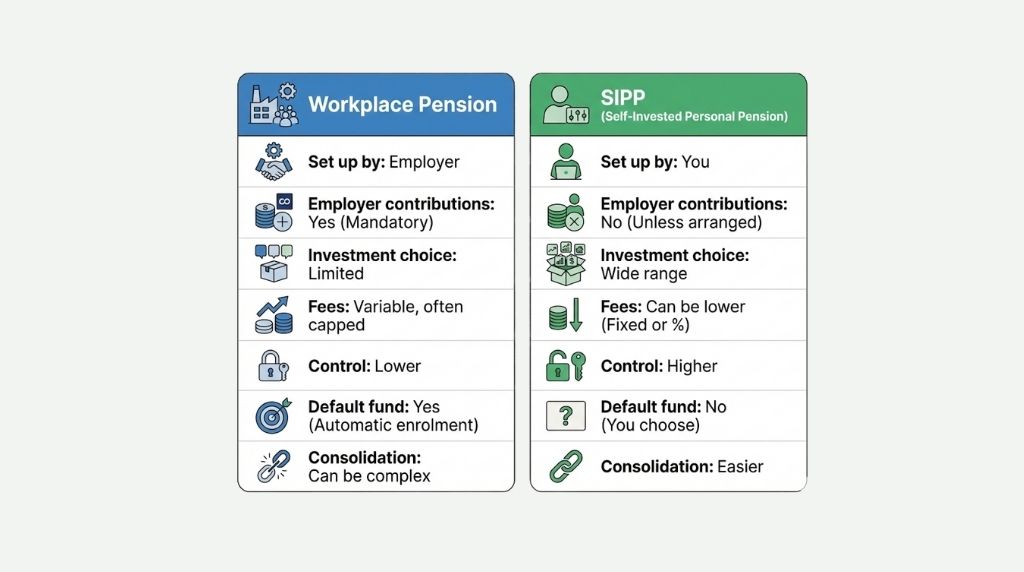

SIPP vs Workplace Pension

A workplace pension is set up by your employer. Your employer must enrol you automatically and contribute at least 3% of your qualifying earnings. Investment options are typically limited to a small number of funds chosen by the pension provider.

A SIPP is a personal arrangement between you and a SIPP provider. There is no employer involvement (although employers can contribute to your SIPP if they choose). You select from thousands of investments and have full control over buying, selling and rebalancing.

Workplace Pension vs SIPP

| Feature | Workplace Pension | SIPP |

|---|---|---|

| Set up by | Your employer | You (personal choice of provider) |

| Employer contributions | Required (minimum 3%) | Optional (employer can contribute) |

| Investment choice | Limited (provider's fund range) | Wide (shares, funds, ETFs, bonds, trusts) |

| Fees | Often low (institutional rates) | Varies by provider (0% to 0.45%+) |

| Control | Minimal | Full control |

| Default fund | Yes (auto-enrolled) | No (you must choose investments) |

| Consolidation | Separate pot per employer | All pensions in one place |

- A SIPP gives you the same tax benefits as a workplace pension but with far more investment choice and control. You can have both a SIPP and a workplace pension at the same time.

How Does a SIPP Work?

A SIPP works in three stages: you contribute money, it grows through investments, and you withdraw it in retirement.

Stage 1: Contributing

When you make a personal contribution to your SIPP, the provider claims basic rate tax relief (20%) from HMRC and adds it to your pot automatically. So if you contribute £800, your provider claims £200 from HMRC, and £1,000 goes into your SIPP.

If you pay higher rate (40%) or additional rate (45%) tax, you can claim the extra relief through your self-assessment tax return. This means a £1,000 SIPP contribution effectively costs a higher rate taxpayer £600 and an additional rate taxpayer £550 (Source: HMRC, 2025/26).

Employers can also contribute directly to your SIPP. Employer contributions are paid gross (no tax relief to claim) and are a tax-deductible business expense, making them highly tax-efficient for both parties.

Stage 2: Investing

Once money is in your SIPP, you choose how to invest it. Most SIPP providers offer access to:

- UK and international shares (individual company stocks)

- Index funds and actively managed funds

- Exchange-traded funds (ETFs)

- Investment trusts

- Government and corporate bonds

- Gilts (UK government bonds)

- Cash deposits

Some full SIPPs also allow commercial property, although this is more complex and typically suited to experienced investors. All investments grow free from UK income tax and capital gains tax inside the SIPP.

Stage 3: Withdrawing

You can access your SIPP from age 55 (rising to age 57 from 6 April 2028) under the Pension Schemes Act 2021 (Source: GOV.UK). You have several options:

Tax-free lump sum: Take up to 25% of your pension pot as a tax-free cash lump sum (known as the Pension Commencement Lump Sum). The maximum tax-free lump sum across all your pensions is £268,275 for 2025/26 (Source: HMRC, Lump Sum Allowance, 2025/26).

Flexi-access drawdown: Keep your money invested and withdraw income as and when you need it. Withdrawals beyond the 25% tax-free amount are taxed at your marginal income tax rate. This is the most popular option for SIPP holders.

Annuity: Use some or all of your pot to buy a guaranteed income for life from an insurance company. Less popular since pension freedoms but still suitable for some retirees who want certainty.

UFPLS (Uncrystallised Funds Pension Lump Sum): Take ad hoc lump sums directly from your pot. Each lump sum is 25% tax-free and 75% taxable. This can be useful for one-off expenses.

Warning: Once you flexibly access taxable income from your SIPP (through drawdown or UFPLS), your annual allowance for future money purchase pension contributions drops to £10,000. This is called the Money Purchase Annual Allowance (MPAA). Plan your withdrawals carefully.

SIPP Tax Rules for 2025/26

Understanding SIPP tax rules is essential for maximising your retirement savings. Here are the key allowances and limits.

Annual Allowance

The standard pension annual allowance is £60,000 for 2025/26, or 100% of your UK earnings, whichever is lower (Source: HMRC, 2025/26). This covers all pension contributions: personal, employer and SIPP combined. Contributions above this limit are subject to an annual allowance charge at your marginal tax rate.

Carry Forward

If you did not use your full annual allowance in the previous three tax years, you can carry forward the unused amount and contribute more than £60,000 in a single year. You must have been a member of a registered pension scheme in those years, and your total contributions cannot exceed 100% of your earnings for the current year (Source: HMRC, Carry Forward Rules).

Tapered Annual Allowance

If your adjusted income exceeds £260,000, your annual allowance reduces by £1 for every £2 above that threshold, down to a minimum of £10,000. This means anyone with adjusted income of £360,000 or more has a £10,000 annual allowance (Source: HMRC, 2025/26).

Tax Relief by Band

SIPP Tax Relief: What You Pay vs What HMRC Adds

| Tax Band | Rate | You Pay (per £1,000 gross) | HMRC Adds | Effective Cost |

|---|---|---|---|---|

| Basic rate | 20% | £800 | £200 | £800 |

| Higher rate | 40% | £600 | £400 | £600 |

| Additional rate | 45% | £550 | £450 | £550 |

| Non-earner | 20% (on £2,880 max) | £2,880 | £720 | £2,880 |

Tax on Withdrawals

When you withdraw from your SIPP, the first 25% is tax-free (up to the Lump Sum Allowance of £268,275). Everything beyond that is added to your taxable income for the year and taxed at your marginal rate. If your only income in retirement is your SIPP drawdown, the first £12,570 falls within your personal allowance and is tax-free.

Inheritance Tax

SIPPs currently sit outside your estate for inheritance tax purposes. If you die before age 75, your beneficiaries can inherit the entire SIPP tax-free. If you die after 75, beneficiaries pay income tax at their marginal rate on withdrawals. Note: the government announced in the Autumn Budget 2025 that pensions will be brought within the scope of inheritance tax from April 2027 (Source: GOV.UK, Autumn Budget 2025).

- SIPP contributions receive tax relief at your marginal rate (20% to 45%). The annual allowance is £60,000, with carry forward available from the previous three years. Plan withdrawals carefully to minimise your income tax bill in retirement.

Who Should Open a SIPP?

SIPPs are not for everyone, but they suit several common situations.

Self-Employed Workers

If you are self-employed, you do not have access to a workplace pension with employer contributions. A SIPP is the most flexible way to save for retirement while benefiting from tax relief. Contributions are made from your net profit and can be deducted from your tax bill through self-assessment.

People Consolidating Old Pensions

If you have changed jobs several times, you may have multiple small workplace pensions. Transferring them into a single SIPP can reduce fees, simplify management and give you better investment options. Check for exit fees and ensure you are not giving up valuable benefits like guaranteed annuity rates before transferring.

Experienced Investors

If you want to invest your pension in individual shares, specific ETFs, or build a diversified portfolio beyond the limited fund range offered by most workplace pensions, a SIPP provides that freedom. Many trading platforms offer SIPPs alongside their ISA and dealing accounts.

Higher and Additional Rate Taxpayers

The tax relief at 40% and 45% makes pension contributions extremely valuable for higher earners. A £10,000 SIPP contribution costs a higher rate taxpayer just £6,000, with the SIPP receiving the full £10,000. See our SIPP vs ISA guide for a detailed comparison.

Parents Saving for Children

Junior SIPPs allow parents or grandparents to contribute up to £2,880 per year (net), which is topped up to £3,600 with 20% tax relief. The money is locked until the child reaches retirement age, giving decades of compound growth.

How to Open a SIPP: Step by Step

Step 1: Choose a SIPP Provider

Compare providers based on fees, investment range, platform quality and customer service. See our best SIPP provider UK guide for detailed reviews. Key providers include:

- Vanguard (low-cost, index funds only, 0.15% capped at £375/year)

- InvestEngine (low-cost ETFs, 0.15% SIPP fee)

- Hargreaves Lansdown (widest fund range, 0.45% capped)

- Interactive Investor (flat fee from £4.99/month, good for larger pots)

Step 2: Open Your Account

You can open a SIPP online in minutes. You will need proof of identity (passport or driving licence), your National Insurance number, and your bank details. Most providers have no minimum to open, although some investment options may have their own minimums.

Step 3: Fund Your SIPP

Set up regular contributions (monthly or ad hoc lump sums). You can also transfer existing pensions into your SIPP. Transfers typically take 4 to 8 weeks. Your provider handles the transfer process, but check for exit fees with your old provider first.

Step 4: Choose Your Investments

Unlike a workplace pension, there is no default fund. You must choose where to invest your money. If you are unsure, a global index fund or a multi-asset fund is a straightforward starting point. As your knowledge grows, you can diversify into individual shares, bonds and specialist funds.

Step 5: Claim Additional Tax Relief

If you are a higher or additional rate taxpayer, remember to claim the extra relief through your self-assessment tax return. Your SIPP provider will reclaim the basic rate (20%) automatically, but the additional 20% or 25% must be claimed separately. See our SIPP tax relief guide for full details.

What Fees Do SIPPs Charge?

SIPP fees vary significantly between providers and can have a major impact on your retirement pot over time. The FCA found that a 1% annual fee difference can reduce a pension pot by over £30,000 over 30 years on £200/month contributions (Source: FCA, 2025).

Common SIPP Fees

Platform/admin fee: An annual charge for holding your SIPP, typically 0% to 0.45% of your pot value, or a flat monthly fee (£4.99 to £12.99). Percentage fees suit smaller pots. Flat fees suit larger pots.

Fund charges (OCF): The ongoing charges figure for the funds you invest in. Index funds typically charge 0.05% to 0.25%. Actively managed funds charge 0.50% to 1.50%.

Dealing fees: Some providers charge per trade when you buy or sell investments. This ranges from free (Trading 212, InvestEngine) to £11.95 per trade (Hargreaves Lansdown).

Drawdown fees: Some providers charge a setup fee or ongoing fee when you enter drawdown. Check this before opening your SIPP, especially if retirement is approaching.

Transfer-out fees: Some older providers charge exit fees if you transfer your SIPP elsewhere. The FCA has pushed for these to be reduced or eliminated.

What Are the Risks of a SIPP?

SIPPs are regulated pension products, but they carry investment risk and require you to make your own decisions.

Investment risk: The value of your SIPP can go down as well as up. Unlike a defined benefit (final salary) pension, there is no guaranteed income. Your retirement income depends entirely on how your investments perform.

Decision-making responsibility: With a workplace pension, a default fund is chosen for you. With a SIPP, you must choose your investments, monitor performance and rebalance when needed. Poor investment choices can significantly reduce your retirement pot.

Locked-in funds: Money in a SIPP cannot be accessed until age 55 (57 from 2028). If you need funds before then, a stocks and shares ISA may be more appropriate for that portion of your savings.

Scam risk: The FCA warns against pension scams that promise early access, guaranteed returns or free pension reviews. If anyone contacts you out of the blue about your pension, it is almost certainly a scam. Check the FCA register before dealing with any firm (Source: FCA, ScamSmart, 2025).

Fee drag: High fees compound over decades. A SIPP charging 1.5% per year will cost significantly more than one charging 0.15% over a 30-year period. Always compare total costs before choosing a provider.

Warning: Be extremely cautious of anyone offering free pension reviews, guaranteed returns, or access to your pension before age 55. These are common signs of pension scams. Always verify a firm on the FCA register at register.fca.org.uk before transferring your pension.

SIPP vs Personal Pension: What Is the Difference?

Both SIPPs and standard personal pensions are individual pension arrangements with the same tax benefits. The key difference is investment choice and control.

A standard personal pension typically offers a limited range of funds chosen by the pension provider. A SIPP offers access to the full range of investments available on the provider's platform, including individual shares, ETFs and investment trusts.

In practice, the line between SIPPs and personal pensions has blurred. Many modern personal pensions now offer broad fund ranges, and some SIPP providers offer ready-made portfolios for investors who want less involvement. The most important thing is to compare fees and fund availability rather than getting caught up in labels. See our SIPP vs personal pension guide for a detailed comparison.

Frequently Asked Questions

SIPP stands for Self-Invested Personal Pension. It is a UK pension that gives you control over how your retirement savings are invested, with access to a wide range of investments including shares, funds, ETFs and bonds.

You can contribute up to £60,000 per year (or 100% of your earnings, whichever is lower) across all your pensions for 2025/26. If you have unused allowance from the previous three tax years, you can carry it forward to contribute more. Even non-earners can contribute £2,880 per year, which becomes £3,600 with basic rate tax relief (Source: HMRC, 2025/26).

Currently at age 55. This rises to age 57 from 6 April 2028 under the Pension Schemes Act 2021. You may be able to access your SIPP earlier if you are in serious ill health. Any scheme or individual claiming to unlock your pension before age 55 is almost certainly a scam.

For most investors who want control over their pension investments, yes. The tax relief alone makes SIPPs extremely valuable, particularly for higher rate taxpayers. However, if you prefer a hands-off approach and your workplace pension has low fees, you may not need a SIPP. The main advantages are wider investment choice, the ability to consolidate old pensions, and potentially lower fees.

Yes. There is no limit on the number of pensions you can hold. Many people use their workplace pension for employer contributions and a SIPP for additional personal contributions with broader investment choice. Your total contributions across all pensions must stay within the £60,000 annual allowance.

If you die before age 75, your SIPP can pass to your nominated beneficiaries completely tax-free. If you die after 75, your beneficiaries pay income tax at their marginal rate on withdrawals. Pensions currently sit outside your estate for inheritance tax, although this is set to change from April 2027 (Source: GOV.UK, Autumn Budget 2025).

In most cases, yes. Contact your SIPP provider and they will handle the transfer process. Before transferring, check for exit fees with your old provider and ensure you are not giving up valuable benefits such as guaranteed annuity rates, employer matching on future contributions, or a protected pension age.

Most SIPP providers have no minimum contribution. You can set up regular monthly payments from as little as £25 with some providers, or make ad hoc lump sum contributions whenever suits you.

You can take 25% of your SIPP tax-free (up to the Lump Sum Allowance of £268,275 across all pensions). The remaining 75% is taxed as income at your marginal rate. If your total income in retirement is below the £12,570 personal allowance, you will not pay any tax on that portion.

SIPP providers are regulated by the FCA and your cash deposits (up to £85,000) are protected by the Financial Services Compensation Scheme (FSCS). Your investments are held in a nominee account separate from the provider's assets, so they are protected if the provider goes bust. However, the value of your investments can go down as well as up.

Related Reading

Explore more investing guides on Smart Investor UK:

- Best SIPP Provider UK - Compare the top SIPP accounts for 2026

- SIPP vs ISA - Which tax wrapper is right for you?

- SIPP Tax Relief Explained - How to claim your full tax relief

- SIPP vs Personal Pension - Key differences explained

- How to Invest in Index Funds UK - Simple investment starting point

- Stocks and Shares ISA Explained - Alternative tax-free wrapper

- Capital Gains Tax on Shares UK - Tax rules outside a SIPP

- How to Start Investing in the UK - Complete beginner's guide

Smart Investor UK is editorially independent. Some links in this article are affiliate links, meaning we may earn a commission if you open an account, at no extra cost to you. This does not affect our editorial independence or the recommendations we make.

Capital at risk. The value of investments can go down as well as up. You may get back less than you invest. Tax treatment depends on individual circumstances and may change. Pension rules may be subject to change. If you are unsure about investing or pension transfers, seek independent financial advice.