Capital gains tax (CGT) in the UK is charged at 18% for basic rate taxpayers and 24% for higher rate taxpayers on profits from selling shares (2025/26). The annual exempt amount is just £3,000, down from £12,300 in 2022/23. Shares held inside an ISA or SIPP are completely exempt. In 2024/25, CGT raised £13.3 billion, and an estimated 264,000 individuals will pay more CGT in 2025/26 following the Autumn Budget 2024 rate increases.

What Is Capital Gains Tax on Shares?

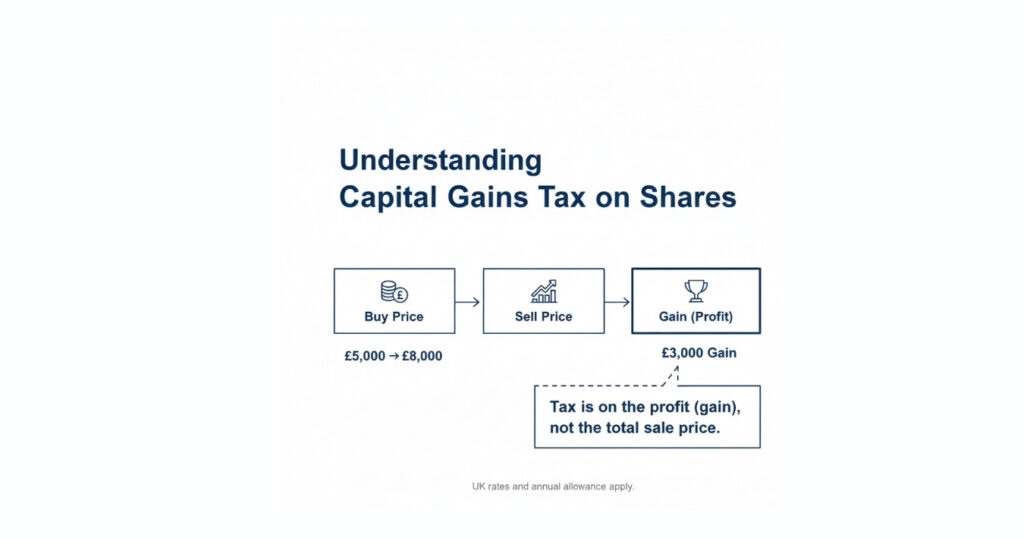

Capital gains tax is a UK tax on the profit you make when you sell shares or other investments for more than you paid for them. You are taxed on the gain, not the total sale price. If you buy shares for £5,000 and sell them for £8,000, you have a taxable gain of £3,000.

CGT only applies when you dispose of an asset. A disposal includes selling shares, gifting shares to someone other than your spouse or civil partner, or transferring shares to a company. You do not pay CGT simply for holding shares or receiving dividends.

The tax applies to shares held in a General Investment Account (GIA). Shares held inside a stocks and shares ISA or SIPP are completely exempt from CGT, which is one of the biggest advantages of tax-efficient wrappers.

In 2022/23, CGT taxpayers disposed of 1.4 million assets worth £188 billion and realised gains of £82 billion, with financial assets accounting for 83% of all disposals (HMRC Capital Gains Tax Statistics, 2025).

- Capital gains tax is charged on profits, not total sale proceeds. Losses can be offset against gains, and shares held within ISAs or SIPPs are fully exempt from CGT.

Capital Gains Tax Rates on Shares 2025/26

The Autumn Budget 2024 significantly increased CGT rates on shares and other non-property assets, aligning them with rates previously charged only on residential property.

Capital Gains Tax Rates (2025/26 vs Pre-Oct 2024)

| Tax Band | CGT Rate 2025/26 | Previous Rate (Pre-Oct 2024) |

|---|---|---|

| Basic rate taxpayer | 18% | 10% |

| Higher / additional rate | 24% | 20% |

| Trusts and PRs | 24% | 20% |

| BADR | 14% (18% from Apr 2026) | 10% |

Source: HMRC / Finance Act 2025

The rate depends on your total taxable income. If income plus taxable gains falls within the basic rate band (£37,700 above the £12,570 personal allowance), you pay 18%. If it pushes you into the higher band, you pay 24% on the portion above the threshold.

These rate increases were announced by Chancellor Rachel Reeves on 30 October 2024, taking immediate effect. They are estimated to affect 264,000 individuals in 2025/26 (GOV.UK) and raise an additional £1.44 billion per year.

Capital Gains Tax Allowance 2025/26

Every individual gets an annual exempt amount (AEA). For 2025/26, this is £3,000. You only pay CGT on gains above this amount.

Capital Gains Tax Annual Exempt Amount Changes

| Tax Year | Annual Exempt Amount | Change |

|---|---|---|

| 2022/23 | £12,300 | — |

| 2023/24 | £6,000 | -51% |

| 2024/25 | £3,000 | -50% |

| 2025/26 | £3,000 | No change |

The allowance has been cut by more than 75% in three years. Many more investors now face a CGT bill. The £3,000 allowance is “use it or lose it” it cannot be carried forward.

Married couples and civil partners each get their own £3,000 allowance, giving a combined £6,000 per year. Transfers between spouses are “no gain, no loss” for CGT purposes.

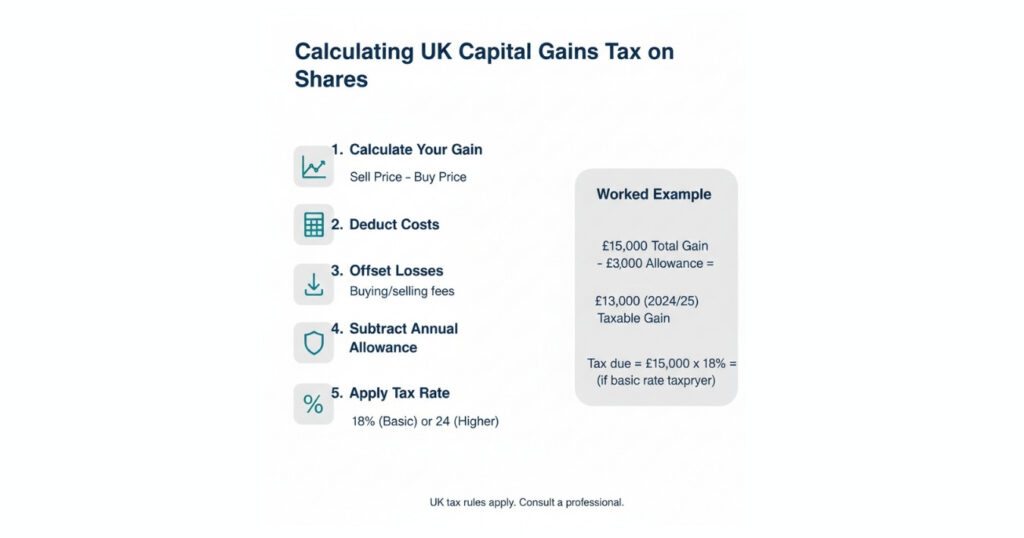

How to Calculate Capital Gains Tax on Shares

Step 1: Work out your gain.

Subtract purchase price (including dealing fees and SDRT) from sale price (minus selling fees).

Step 2: Deduct allowable costs.

Broker commissions, platform fees, and the 0.5% stamp duty reserve tax paid on purchase.

Step 3: Offset any losses.

Losses from other share sales in the same year offset gains. Unused losses carry forward indefinitely.

Step 4: Deduct the annual exempt amount.

Subtract the £3,000 AEA from your net gain.

Step 5: Apply the correct rate.

Tax the remainder at 18% (basic) or 24% (higher) depending on your income.

Worked Example: £15,000 Capital Gain

| Item | Amount |

|---|---|

| Gross gain | £15,000 |

| Less: Annual exempt amount | -£3,000 |

| Taxable gain | £12,000 |

| CGT at 18% (basic rate) | £2,160 |

| CGT at 24% (higher rate) | £2,880 |

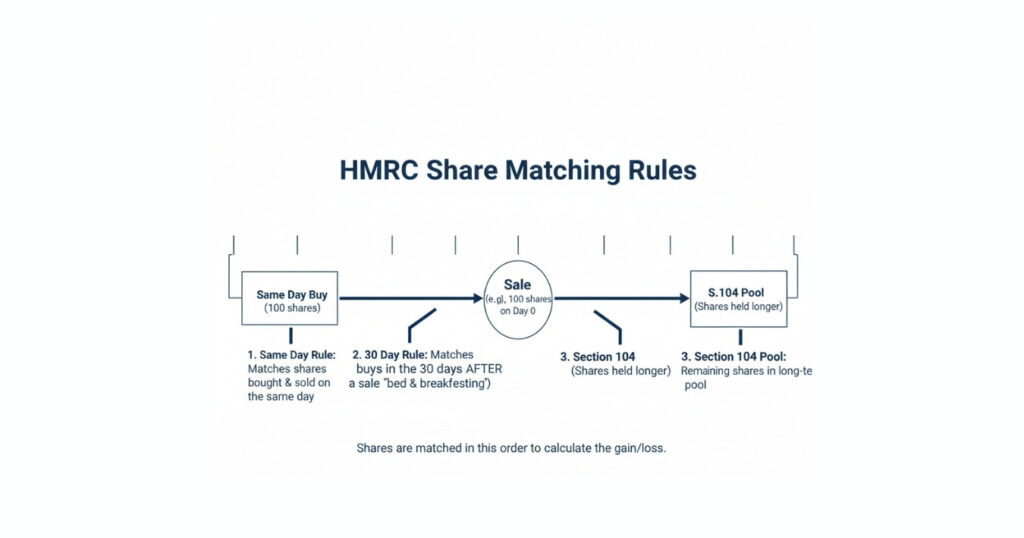

Matching Rules for Share Sales

When you sell shares bought in multiple batches at different prices, HMRC uses specific matching rules:

1. Same-day rule: Shares bought on the same day as the sale.

2. 30-day rule: Shares bought in the 30 days following the sale (the “bed and breakfasting” rule).

3. Section 104 pool: A weighted average of all your remaining shares of that class.

The 30-day rule prevents you from selling shares to crystallise a loss and immediately buying them back. If you repurchase the same shares within 30 days, the sale is matched to the repurchase.

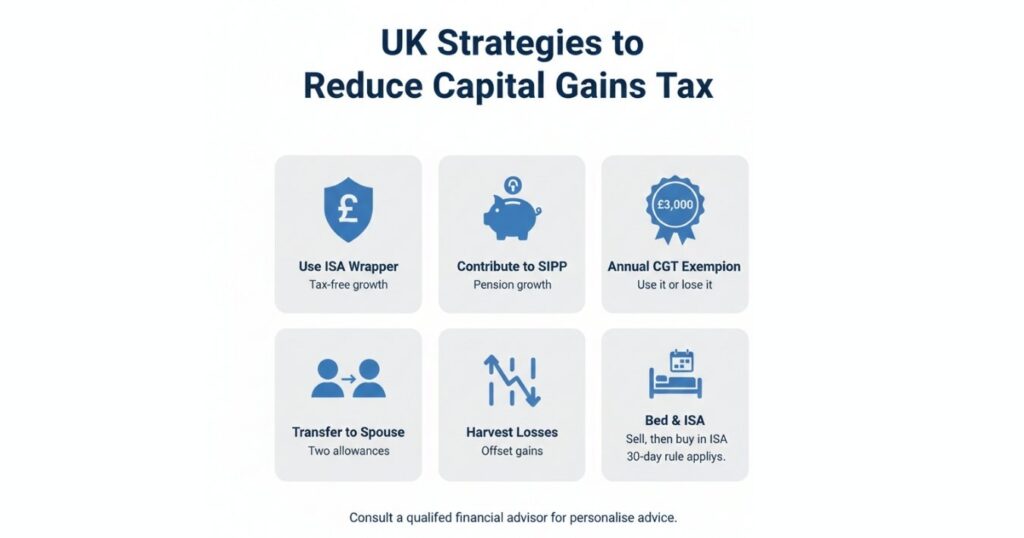

How to Reduce Capital Gains Tax on Shares (Legally)

Use Your Use Your ISA Allowance

The most effective strategy is to hold investments inside a stocks and shares ISA. Any gains within an ISA are completely tax-free. You can contribute up to £20,000 per year.

If you already hold shares in a taxable account, consider “Bed and ISA”: sell shares in your GIA and repurchase them within your ISA. You may trigger a CGT charge on the sale, but all future gains will be tax-free.

Use Your SIPP

Shares inside a pension () are exempt from CGT. You also receive tax relief on contributions, making pensions extremely tax-efficient.

Use your annual exempt amount every year. Crystallise gains up to £3,000 each year. Wait at least 30 days before repurchasing the same shares, or buy a similar but not identical investment.

Transfer shares to your spouse. Transfers to spouses/civil partners are CGT-exempt. Together, a couple can realise £6,000 in tax-free gains per year.

Harvest losses. Sell any shares standing at a loss before the tax year end to offset gains. Losses carry forward indefinitely.

- The most effective way to avoid capital gains tax on shares is to hold them inside a Stocks and Shares ISA, where all gains are permanently tax-free.

When Do You Need to Report Capital Gains Tax?

If gains exceed £3,000 in a tax year, you must report through Self Assessment. The deadline is 31 January following the tax year end. For 2025/26, the deadline is 31 January 2027.

You may also need to report if total disposal proceeds exceed four times the AEA (£12,000 for 2025/26), even with no taxable gain.

CGT on shares is reported via Self Assessment (form SA108). If you do not normally file Self Assessment, you can use HMRC’s online Capital Gains Tax service. Unlike property CGT, there is no 60-day reporting requirement for share disposals.

Capital Gains Tax vs Other Taxes on Investments

UK Investment Taxes (2025/26)

| Tax | Applies To | Rate (2025/26) | Allowance |

|---|---|---|---|

| Capital gains tax | Profits from selling shares | 18% / 24% | £3,000 |

| Dividend tax | Dividend income | 8.75% / 33.75% / 39.35% | £1,000 |

| Income tax (interest) | Bond/savings interest | 20% / 40% / 45% | £1,000 / £500 PSA |

| SDRT | Buying UK shares | 0.5% | None |

All of these taxes can be avoided by investing within an ISA. For dividend taxation, see dividend tax UK.

How Many People Pay Capital Gains Tax?

In 2022/23, 348,000 individuals paid CGT, compared to 34.6 million income tax payers (HMRC, 2025). The number is expected to grow significantly as allowances shrink.

CGT raised £13.3 billion in 2024/25. The Office for Budget Responsibility estimates £20.3 billion in 2025/26 approximately 1.6% of all tax receipts and £705 per UK household (OBR, 2025). Most revenue comes from a small number of high-value disposals: financial assets accounted for 77% of all realised gains in 2022/23.

- The CGT allowance has fallen significantly in recent years. Many investors who previously did not need to consider capital gains tax now need to plan carefully or use ISAs to shelter investments.

Frequently Asked Questions

No. Shares held inside a stocks and shares ISA are completely exempt from capital gains tax, regardless of the size of the gain.

In 2025/26, the annual exempt amount is £3,000. You only pay capital gains tax on gains above this threshold. Married couples each receive their own £3,000 allowance.

Capital gains tax is 18% for basic rate taxpayers and 24% for higher rate taxpayers.

Yes. Losses can offset gains in the same tax year. Unused losses can be carried forward indefinitely but must be reported to HMRC.

Capital gains tax is paid through Self Assessment by 31 January following the end of the tax year.

Generally yes. Gifting shares to someone other than your spouse or civil partner is treated as a disposal at market value. Transfers between spouses are exempt.

If you sell and repurchase the same shares within 30 days, the sale is matched against the repurchase rather than your original holding for capital gains tax purposes.

No. The UK does not offer reduced capital gains tax rates for longer holding periods. The same rates apply regardless of how long the shares are held.

You report gains through your Self Assessment tax return, typically using form SA108, or via HMRC’s online capital gains reporting service.

If you have unused capital gains allowance, crystallising gains before 5 April may allow you to use the £3,000 exemption before it expires.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or tax advice. Tax rules depend on individual circumstances and may change. The value of your investments can go down as well as up. Always consider your own financial situation and consult a qualified tax adviser if unsure about your CGT obligations.