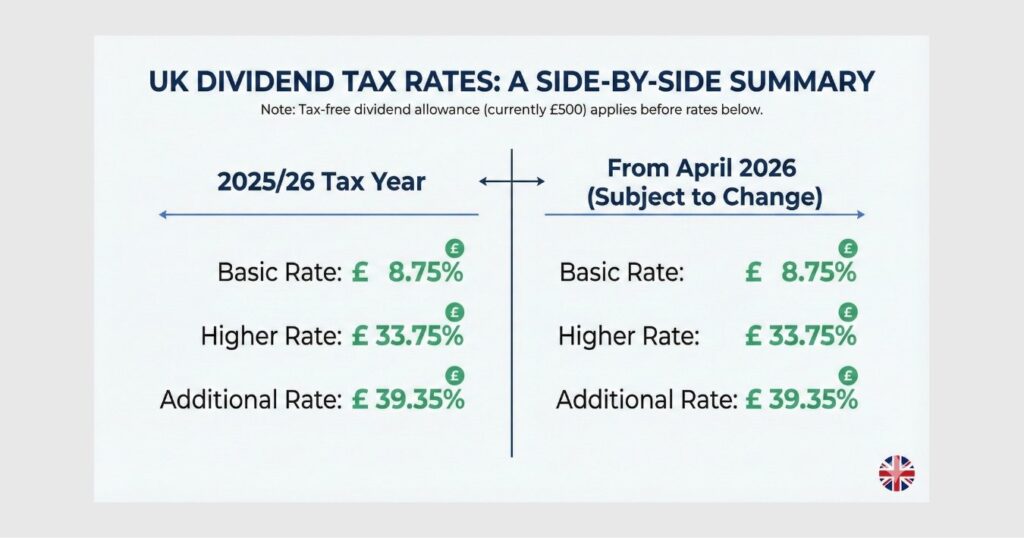

In 2025/26, UK dividend tax rates are 8.75% (basic rate), 33.75% (higher rate), and 39.35% (additional rate). You get a £500 tax-free dividend allowance, down from £5,000 in 2017. From April 2026, rates rise by 2 percentage points to 10.75% and 35.75% (GOV.UK, November 2025). A record 3.67 million individuals are expected to pay dividend tax in 2024/25 nearly double the 1.9 million in 2022/23 (HMRC/Quilter, 2025). Dividends inside an ISA or SIPP are completely tax-free.

What Is Dividend Tax?

Dividend tax is the income tax you pay on dividend income received from owning shares in a company. When a company distributes part of its profits to shareholders, those payments are called dividends and in the UK, they are subject to specific tax rates that are lower than standard income tax rates.

Unlike salary or wages, dividends are not subject to National Insurance contributions (NICs). This is one reason why company directors often pay themselves a combination of a low salary and dividends it is more tax-efficient than taking everything as salary.

You receive UK dividends gross, meaning no tax is deducted at source. It is your responsibility to report dividend income above the allowance to HMRC and pay any tax owed, typically through Self Assessment or a PAYE tax code adjustment.

Dividend tax applies to dividends received on shares held outside of tax-efficient wrappers. Dividends received inside a stocks and shares ISA or a pension (such as a SIPP) are completely exempt from tax and do not count towards your allowance.

Dividend Tax Rates 2025/26

The rate you pay on dividends depends on your overall income tax band. Dividend income is added on top of your other income (salary, pensions, rental income) to determine which band applies.

Dividend Tax Bands and Rates (2025/26 and From April 2026)

| Income Tax Band | Taxable Income (2025/26) | Dividend Rate (2025/26) | From April 2026 |

|---|---|---|---|

| Basic rate | £12,571 – £50,270 | 8.75% | 10.75% |

| Higher rate | £50,271 – £125,140 | 33.75% | 35.75% |

| Additional rate | Over £125,140 | 39.35% | 39.35% (no change) |

Source: GOV.UK, Changes to Tax Rates for Property, Savings & Dividend Income, November 2025

From 6 April 2026, the basic rate rises from 8.75% to 10.75% and the higher rate from 33.75% to 35.75%. The additional rate remains at 39.35%. The government estimates this increase will raise £280 million in additional tax in 2026/27, rising to £1.39 billion by 2030/31 (GOV.UK).

These rates are significantly lower than the equivalent income tax rates (20%, 40%, and 45%), reflecting the fact that companies pay corporation tax on their profits before distributing dividends. This avoids full double taxation though it does not eliminate it entirely, since corporation tax at 25% has already been deducted before dividends reach shareholders.

- Dividend tax rates increase by 2 percentage points from April 2026 for basic and higher rate taxpayers. Planning the timing of dividend payments may help manage future tax exposure.

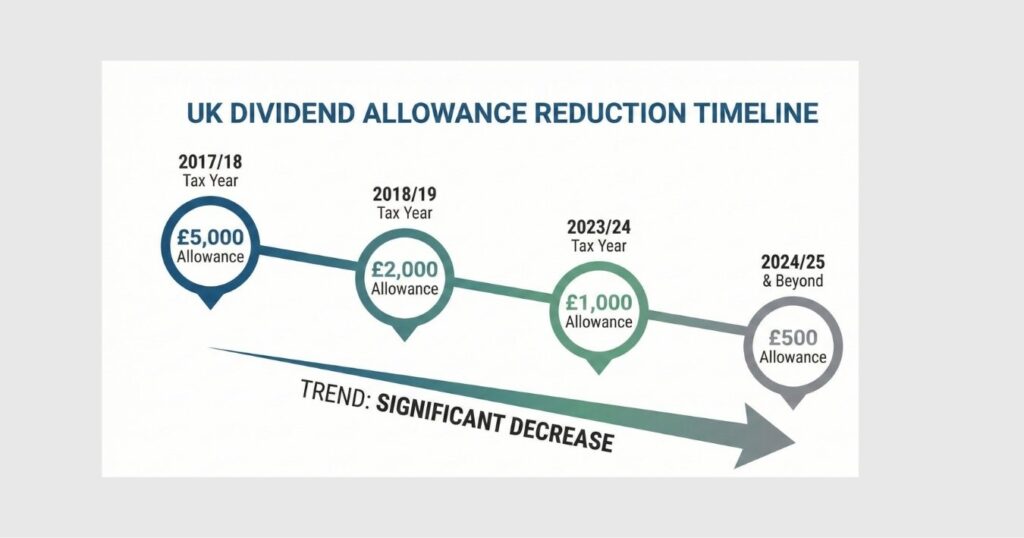

Dividend Allowance 2025/26

The dividend allowance is the amount of dividend income you can receive each year before paying any tax. For 2025/26, the allowance is £500.

Dividend Allowance Reductions Over Time

| Tax Year | Dividend Allowance | Change |

|---|---|---|

| 2016/17 – 2017/18 | £5,000 | — |

| 2018/19 – 2022/23 | £2,000 | -60% |

| 2023/24 | £1,000 | -50% |

| 2024/25 – 2025/26 | £500 | -50% |

The allowance has been cut by 90% in less than a decade, from £5,000 to just £500. This means investors who previously had comfortable headroom now face a tax bill on relatively modest dividend income.

If dividends are your only income, you can also use your £12,570 personal allowance. This means you could receive up to £13,070 in dividend income before paying any tax (£12,570 personal allowance plus £500 dividend allowance). However, if you have a salary or pension that already uses up your personal allowance, only the £500 dividend allowance applies to your dividend income.

The dividend allowance works as a zero-rate band, not a deduction. This means your dividends still count as income for the purpose of determining your tax band, even though the first £500 is taxed at 0%.

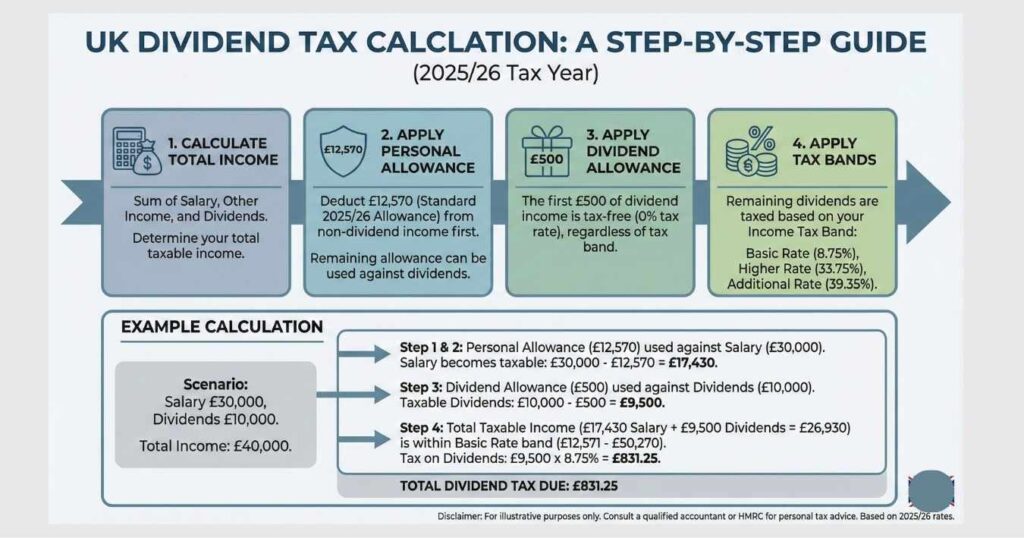

How to Calculate Dividend Tax

Calculating your dividend tax involves three steps:

Step 1: Add up all your income.

Combine your salary, pension, rental income, and dividend income to find your total income for the year.

Step 2: Apply your allowances.

Deduct your personal allowance (£12,570) and dividend allowance (£500) from the relevant portions of income.

Step 3: Apply the correct dividend tax rate

based on which income tax band your dividend income falls into.

Worked Example: Basic Rate Taxpayer

Dividend Tax Worked Example (Basic Rate Taxpayer)

| Detail | Amount |

|---|---|

| Salary | £30,000 |

| Dividend income | £5,000 |

| Total income | £35,000 |

| Less: Personal allowance (applied to salary) | -£12,570 |

| Taxable salary | £17,430 (taxed at 20% = £3,486) |

| Dividend allowance | -£500 |

| Taxable dividends | £4,500 |

| Dividend tax at 8.75% (basic rate) | £393.75 |

Worked Example: Higher Rate Taxpayer

Dividend Tax Worked Example (Higher Rate Taxpayer)

| Detail | Amount |

|---|---|

| Salary | £55,000 |

| Dividend income | £8,000 |

| Total income | £63,000 |

| Dividend allowance | -£500 |

| Taxable dividends | £7,500 |

| Dividend tax at 33.75% (all in higher rate band) | £2,531.25 |

In the second example, the investor pays over £2,500 in dividend tax on just £8,000 of dividends. This illustrates why higher rate taxpayers benefit enormously from holding dividend-paying shares inside an ISA.

How Many People Pay Dividend Tax?

The number of people caught by the dividend tax net has surged following the allowance cuts:

Individuals Paying Dividend Tax

| Year | Individuals Paying Dividend Tax | Change |

|---|---|---|

| 2022/23 | 1.9 million | — |

| 2023/24 (est.) | 3.08 million | +62% |

| 2024/25 (est.) | 3.67 million | +19% |

Source: HMRC data via Quilter Freedom of Information request, 2025

Over 1.3 million additional individuals became liable for dividend tax in just two years as a direct result of the allowance being cut from £2,000 to £500. Of particular note, more than 1.1 million basic rate taxpayers were expected to owe dividend tax in 2024/25, many for the first time (HMRC/Quilter, 2025).

The reduction in the allowance is forecast to raise £450 million in 2024/25, climbing to £810 million in 2025/26, £860 million in 2026/27, and £940 million in 2027/28 (HMRC).

EQ (Equiniti), one of the UK's largest share registrars, analysed 7.8 million individual shareholder accounts and found that 88.7% of shareholders received dividends of £250 or less in 2024/25. However, the remaining shareholders receiving over £500 per year now face a reporting and tax obligation that many are encountering for the first time.

- Around 3.67 million individuals are now expected to pay dividend tax, nearly double the figure from two years earlier. Recent allowance reductions have brought over one million additional basic rate taxpayers into the dividend tax system.

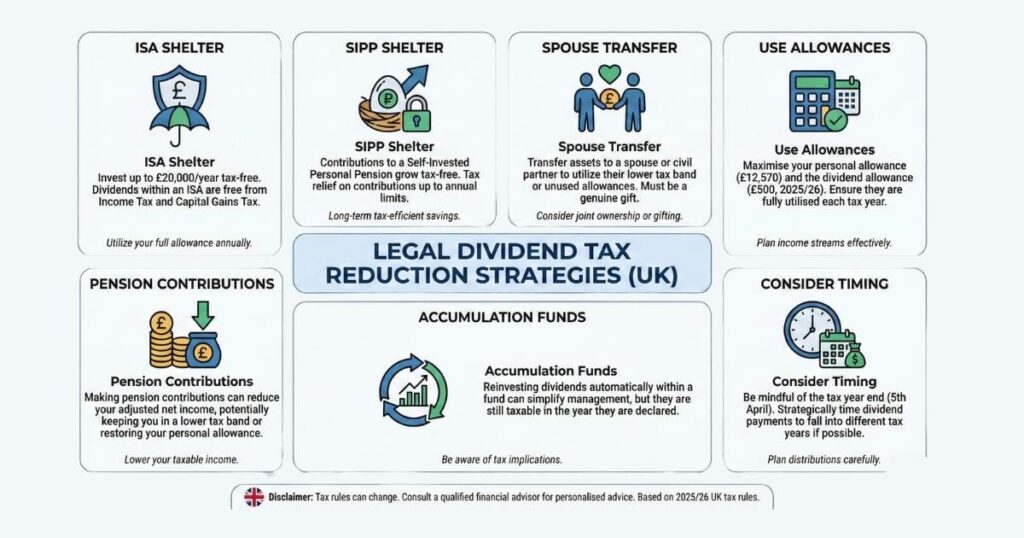

How to Reduce or Avoid Dividend Tax (Legally)

There are several legitimate strategies to minimise your dividend tax bill:

Hold Shares Inside an ISA

The most powerful strategy for investors. Dividends received inside a stocks and shares ISA are completely tax-free no dividend tax, no capital gains tax, and no need to report to HMRC. You can invest up to £20,000 per year in ISAs.

For every £1,000 of dividend income, using an ISA instead of a taxable account saves you £87.50 (basic rate) or £337.50 (higher rate) per year at current 2025/26 rates. These savings increase from April 2026 when rates rise.

For more details, see our guide to the best stocks and shares ISA.

Hold Shares Inside a Pension (SIPP)

Dividends received inside a SIPP are also completely tax-free. Additionally, you receive tax relief on pension contributions (up to 100% of your earnings or £60,000 per year, whichever is lower), making this a doubly tax-efficient strategy. The trade-off is that you cannot access pension funds until age 55 (rising to 57 from 2028).

For more information, see our best SIPP guide.

Use Your Dividend Allowance

Ensure you use the full £500 allowance each year. If you hold shares jointly with a spouse or civil partner, you may each be able to claim your own £500 allowance, giving £1,000 of tax-free dividends between you.

Transfer Shares to Your Spouse

If your spouse or civil partner is in a lower tax band or is not using their own personal allowance and dividend allowance transferring shares to them can reduce the overall family tax bill. For example, if one partner is a higher rate taxpayer paying 33.75% and the other is a basic rate taxpayer paying 8.75%, transferring shares could save 25 percentage points on the dividend tax.

Make Pension Contributions to Lower Your Tax Band

Pension contributions reduce your taxable income. If your income is just above the higher rate threshold (£50,270), making pension contributions could bring you back into the basic rate band, where dividend tax is 8.75% instead of 33.75%. A £5,000 pension contribution could reduce your dividend tax bill by up to £1,250 per year.

Consider Accumulation Funds

Rather than investing in individual dividend-paying shares, you could invest in accumulation fund units, which automatically reinvest dividends within the fund rather than distributing them to you. Within an ISA this makes no tax difference, but outside an ISA, accumulation funds defer the dividend tax until you sell, at which point you pay capital gains tax instead (potentially at a lower effective rate if your CGT allowance is unused).

- The single most effective way to avoid dividend tax is to hold your shares inside an ISA. All dividends within an ISA are permanently tax-free and never need reporting.

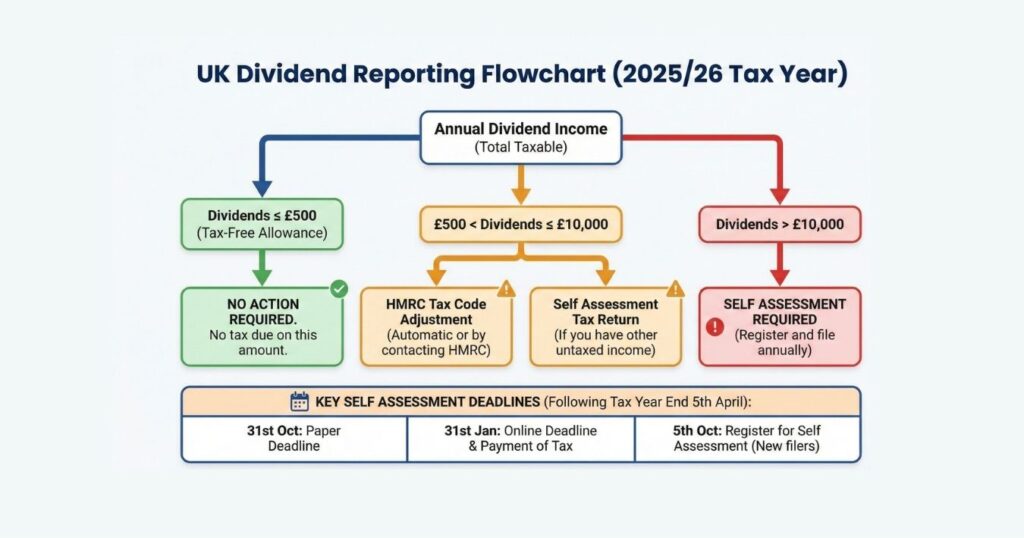

How to Report and Pay Dividend Tax

Dividends within the £500 allowance: No action required. You do not need to tell HMRC.

Dividends between £500 and £10,000: You can either ask HMRC to adjust your PAYE tax code (so the tax is collected from your salary or pension) or file a Self Assessment tax return. Contact HMRC by 5 October following the end of the tax year.

Dividends over £10,000: You must file a Self Assessment tax return. The deadline for online returns is 31 January following the tax year end (31 January 2027 for 2025/26 income).

You should keep records of all dividend payments received, including dividend vouchers or statements from your broker or investment platform. Most platforms provide an annual tax summary showing total dividends received during the tax year.

Dividends received inside an ISA do not need to be reported, regardless of the amount. They are completely outside the tax system.

Dividend Tax vs Other Investment Taxes

Dividends are one of several taxes that apply to investment income. Here is how they compare:

UK Investment Taxes and ISA Exemption (2025/26)

| Tax | What It Applies To | 2025/26 Rate | Allowance | ISA Exempt? |

|---|---|---|---|---|

| Dividend tax | Dividends from shares | 8.75% / 33.75% / 39.35% | £500 | Yes |

| Capital gains tax | Profits from selling shares | 18% / 24% | £3,000 | Yes |

| Income tax (interest) | Interest on bonds/savings | 20% / 40% / 45% | £1,000 / £500 PSA | Yes |

| Stamp duty (SDRT) | Buying UK shares | 0.5% | None | No |

All of these taxes (except SDRT) can be avoided by investing within a stocks and shares ISA. This makes ISAs the cornerstone of tax-efficient investing in the UK.

For more on capital gains tax, see our pillar guide: capital gains tax on shares UK.

What Is Changing From April 2026?

The Autumn Budget 2025 announced a 2 percentage point increase in dividend tax rates from 6 April 2026:

Dividend Tax Rate Changes

| Rate | 2025/26 (Current) | From April 2026 | Increase |

|---|---|---|---|

| Basic rate | 8.75% | 10.75% | +2pp |

| Higher rate | 33.75% | 35.75% | +2pp |

| Additional rate | 39.35% | 39.35% | No change |

Source: GOV.UK, Changes to Tax Rates for Property, Savings & Dividend Income, November 2025

The dividend allowance remains at £500 it is not being changed.

For a basic rate taxpayer receiving £5,000 in dividends (after the £500 allowance), the annual tax increase is £90 (from £393.75 to £483.75). For a higher rate taxpayer, the same £4,500 of taxable dividends costs an additional £90 (from £1,518.75 to £1,608.75).

These increases make it more important than ever to shelter dividend income inside an ISA or pension where possible. For those who can control the timing of dividend payments (such as company directors), it may be worth considering bringing forward dividends before 6 April 2026.

Frequently Asked Questions

The first £500 of dividend income is tax-free under the dividend allowance. If you have no other income, you can also use your £12,570 personal allowance, allowing up to £13,070 in total before tax is due.

No. Dividends received inside a Stocks and Shares ISA are completely tax-free and do not need to be reported to HMRC.

Basic rate: 8.75%. Higher rate: 33.75%. Additional rate: 39.35%.

You may need to file a Self Assessment return if your dividends exceed £10,000 per year. For amounts between £500 and £10,000, HMRC may collect the tax through your tax code or require a return.

Dividend tax is a type of income tax but charged at different rates. Companies pay corporation tax before distributing dividends, which is why dividend tax rates are lower than standard income tax rates.

No. Reinvested dividends are still taxable in the year they are paid, even if automatically reinvested. Dividends within an ISA or SIPP are tax-free.

Dividends are taxed in the same way as for other shareholders. Many directors take a salary up to the personal allowance and then receive dividends, which are taxed at dividend tax rates.

Yes. Dividend income is usually split equally between joint holders, and each person applies their own £500 dividend allowance and tax bands.

Yes. UK tax residents pay UK dividend tax on overseas dividends. You may be able to claim a credit for foreign withholding tax deducted.

Dividend tax is paid through Self Assessment by 31 January following the end of the tax year.

Related Reading

Capital Gains Tax on Shares UK How CGT works alongside dividend tax

Stocks and Shares ISA Explained Shelter your dividends from tax

Best Stocks and Shares ISA Top platforms for dividend investors

Best Dividend Stocks UK High-yield income shares to consider

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or tax advice. Tax rules depend on individual circumstances and may change. The value of your investments can go down as well as up. Always consider your own financial situation and consult a qualified tax adviser or accountant if you are unsure about your dividend tax obligations.